- 製造業出身のデータサイエンティストがお送りする記事

- 今回は時系列解析手法のSARIMAモデルを試してみた

はじめに

過去に時系列解析に関しては何個か整理しておりますので、興味ある方は参照して頂けますと幸いです。

SARIMAモデルとは

SARIMAモデルを説明する前に、ARIMAモデルについて整理します。

ARIMAモデルとは、「autoregressive integrated moving average」の略で、自己回帰モデル(ARモデル)、移動平均モデル(MAモデル)、和分モデル(Iモデル)の3モデルを組み合わせたモデルです。

SARIMAモデルとは、「Seasonal AutoRegressive Integrated Moving Average」の略で、ARIMAモデルに「季節的な周期パターン」を加えたモデルです。

つまり、季節変動があるデータに対してARIMAモデルを拡張した手法が、SARIMAモデルです。具体的には、時系列方向にARIMAモデルを使い、かつ、周期方向にもARIMAモデルを使っているモデルです。

SARIMAモデル

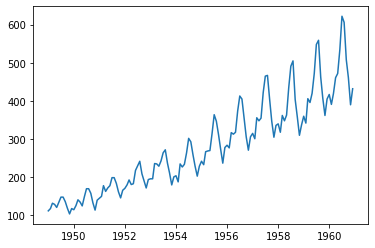

今回も使用したデータは、月ごとの飛行機の乗客数データです。

# ライブラリーのインポート

import warnings

warnings.filterwarnings('ignore')

import itertools

import matplotlib.pyplot as plt

import numpy as np

import pandas as pd

import statsmodels.api as sm

from plotly import tools

from plotly.graph_objs import Bar, Figure, Layout, Scatter

from plotly.offline import init_notebook_mode, iplot

from sklearn.metrics import mean_squared_error

from statsmodels.tsa.arima_model import ARIMA, ARMA

from statsmodels.tsa.statespace.sarimax import SARIMAX

import plotly

init_notebook_mode(connected=True)

save_image = None # 'png' if save image

# https://stat.ethz.ch/R-manual/R-devel/library/datasets/html/AirPassengers.html

df = pd.read_csv('../data/AirPassengers.csv')

# float型に変換

df['#Passengers'] = df['#Passengers'].astype('float64')

df = df.rename(columns={'#Passengers': 'Passengers'})

# datetime型にしてインデックスにする

df.Month = pd.to_datetime(df.Month)

df = df.set_index("Month")

# データの中身を確認

df.head()

# データの可視化

plt.plot(df.Passengers)

plt.show()

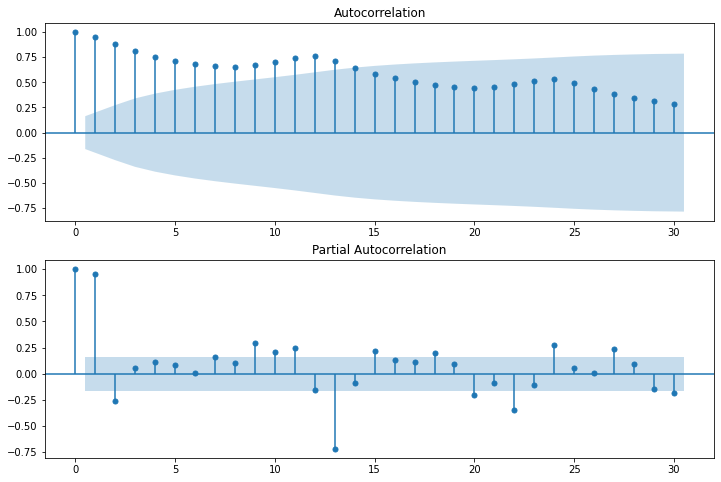

# コレログラム

fig = plt.figure(figsize=(12,8))

ax1 = fig.add_subplot(211)

fig = sm.graphics.tsa.plot_acf(df.Passengers, lags=30, ax=ax1)

ax2 = fig.add_subplot(212)

fig = sm.graphics.tsa.plot_pacf(df.Passengers, lags=30, ax=ax2)

次に定常性の確認を行います。

今回は、adfuller を用いて、Dickey-Fuller 検定を行いました。

res = sm.tsa.stattools.adfuller(df.Passengers)

print('p-value = {:.4}'.format(res[1]))

# p-value = 0.9919

Passengers: p-value > 0.1なので有意水準10%で帰無仮説(定常性を満たす)は棄却されず、定常ではない事が分かります。

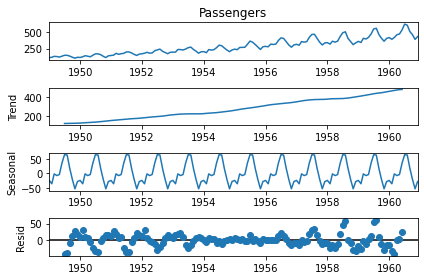

次に、成分分解を行ってみます。

res = sm.tsa.seasonal_decompose(df["Passengers"])

fig = res.plot()

本当は差分系列や対数差分系列など、細かい確認が必要なのですが、今回はSARIMAモデルを試すことが重要なので進めます。

それでは、SARIMAモデルを構築します。

# 学習と評価データに分割

df_train = df[df.index < '1957-04-01']

df_test = df[df.index >= '1957-04-01']

ts = df.Passengers

ts_train = df_train.Passengers

ts_test = df_test.Passengers

def eval_model(ts_train, ts_test, result):

train_pred = result.predict()

test_pred = result.forecast(len(ts_test))

test_pred_ci = result.get_forecast(len(ts_test)).conf_int()

train_rmse = np.sqrt(mean_squared_error(ts_train, train_pred))

test_rmse = np.sqrt(mean_squared_error(ts_test, test_pred))

print('RMSE(train):\t{:.5}\nRMSE(test):\t{:.5}'.format(

train_rmse, test_rmse))

return train_pred, test_pred, test_pred_ci

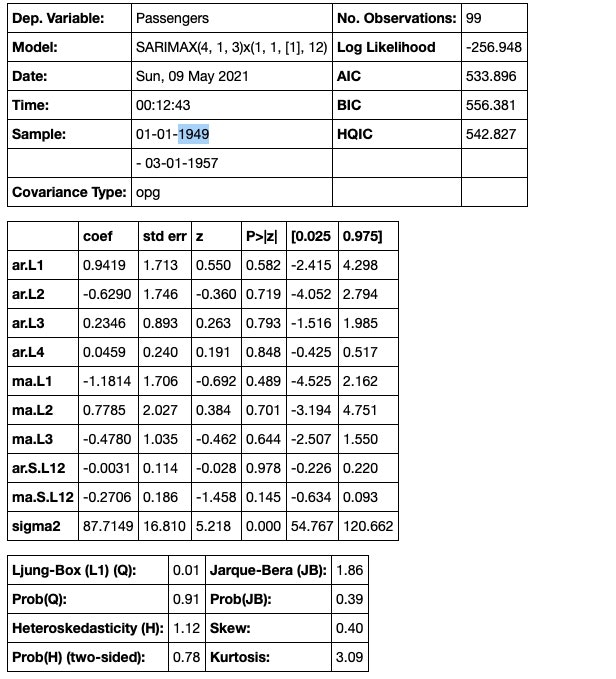

order=(4,1,3)

seasonal_order=(1,1,1,12)

model = SARIMAX(

ts_train,

order=order,

seasonal_order=seasonal_order,

enforce_stationarity=False,

enforce_invertibility=False)

result = model.fit()

train_pred, test_pred, test_pred_ci = eval_model(ts_train, ts_test, result)

result.summary()

# RMSE(train): 17.811

# RMSE(test): 27.347

各パラメータは「arma_order_select_ic」などを用いて決めると良いと思います。

次は予測を行いたいと思います。

train_pred = result.predict()

test_pred = result.forecast(len(ts_test))

test_pred_ci = result.get_forecast(len(ts_test)).conf_int()

train_rmse = np.sqrt(mean_squared_error(df_train, train_pred))

test_rmse = np.sqrt(mean_squared_error(df_test, test_pred))

print('RMSE(train): {:.5}\nRMSE(test): {:.5}'.format(train_rmse, test_rmse))

# RMSE(train): 17.811

# RMSE(test): 27.347

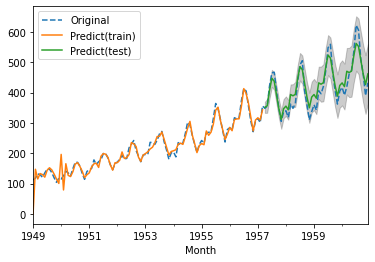

最後に可視化してみようと思います。

fig, ax = plt.subplots()

df.Passengers.plot(ax=ax, label='Original', linestyle="dashed")

train_pred.plot(ax=ax, label='Predict(train)')

test_pred.plot(ax=ax, label='Predict(test)')

ax.fill_between(

test_pred_ci.index,

test_pred_ci.iloc[:, 0],

test_pred_ci.iloc[:, 1],

color='k',

alpha=.2)

ax.legend()

さいごに

最後まで読んで頂き、ありがとうございました。

時系列解析手法のSARIMAモデルを試してみた。

訂正要望がありましたら、ご連絡頂けますと幸いです。