order_value

order_valueは,銘柄と取引額を指定して注文する関数です.

order_value(asset, amount, style=OrderType)

asset: Equity/Future オブジェクト

amount: 取引額.正であればLong,負であればShort.

style: 注文方法(指定方法はorderを参照)

アルゴリズム例

#Quantopian Algorithm で orderのコードを一箇所だけ変えました.

def initialize(context):

# AAPL

context.security = sid(24)

# rebalance 関数を毎日クローズ一分前(15:59)に実行するように指定

schedule_function(rebalance,

date_rule=date_rules.every_day(),

time_rule=time_rules.market_close(minutes = 1))

def rebalance(context, data):

# 過去5日間の平均を取得して,今日の価格よりも1%大きければLong

# 今日価格が移動平均より小さければ,ポジションクローズする

# 過去5日間のヒストリカルデータを取得.

# 【注意】https://www.quantopian.com/help#ide-history に説明があるとおり,

# 日中にヒストリカルデータを複数日分取得すると,

# 「過去4日分と今現在の価格」が取得できます.現在価格はhistorical data 同様,アジャストされた価格です.

price_history = data.history(

context.security,

fields='price',

bar_count=5,

frequency='1d'

)

# price_historyを出力

# log.info(price_history)

# 平均値

average_price = price_history.mean()

# 現在の価格

current_price = data.current(context.security, 'price')

# log.info(current_price)

# 注文しようとしている銘柄が,現在上場されているか確認

if data.can_trade(context.security):

# 平均値より,1%大きければ,Long

if current_price > (1.01 * average_price):

# 成り行きで10株買う

order_value(context.security, 1000) # ←変更箇所

log.info("Buying %s" % (context.security.symbol))

# 平均値より小さければ,ポジションをクローズ

elif current_price < average_price:

# 0と注文することでポジションを精算することになる

order_target(context.security, 0)

log.info("Selling %s" % (context.security.symbol))

# 平均値と現在価格を描画

record(current_price=current_price, average_price=average_price)

メモ

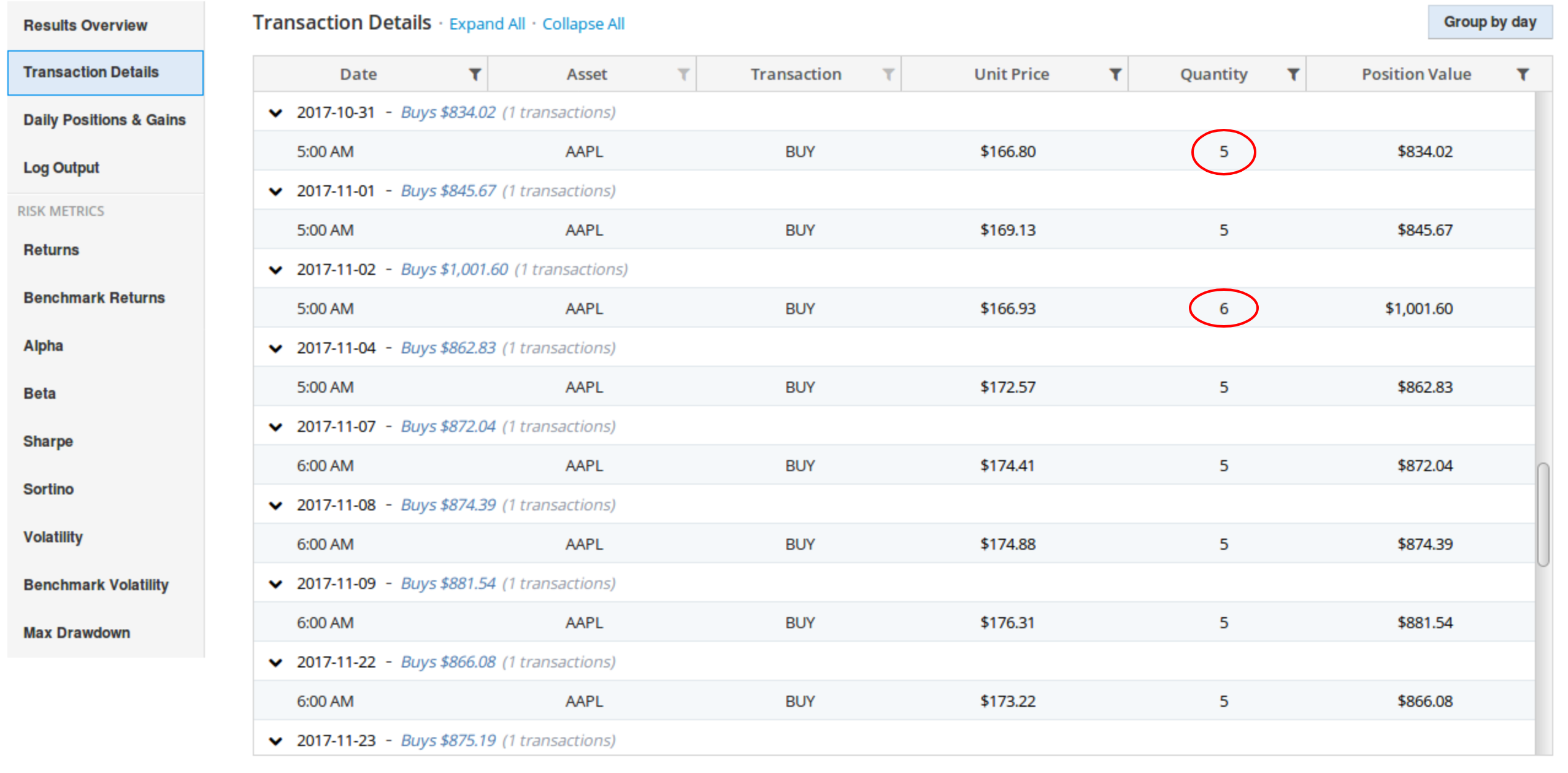

このアルゴリズムは,条件にあえば1000ドル分買い足して行くというアルゴリズムです.1000ドル分とは,1000ドルを超えないオーダーという意味になります.例えば,AAPLが105ドルであれば,9株注文してくれます.株数を確認したい場合は,run full backtest を実行した後,Transaction Detailsを見ると確認できます.

(株価に合わせて,よしなに5株買ったり6株買ったりしている↓)

気が向いた時に,アルゴリズムの注文方法を少しずつ書いていこうと思います.

次はorder_percentです.

他のオーダー方法

#Quantopian Algorithm で order

#Quantopian Algorithm で order_percent

#Quantopian Algorithm で order_target

#Quantopian Algorithm で order_target_value