『経済・ファイナンスデータの計量時系列分析』

の章末問題で「コンピュータを用いて」とあるものをRで解いています。

2.5

- (1)

library(forecast)

data<-read.table("economicdata.txt",header=T)

ar4<-Arima(diff(log(data$indprod))*100, order=c(4, 0, 0))

ma3<-Arima(diff(log(data$indprod))*100, order=c(0, 0, 3))

arma1_1<-Arima(diff(log(data$indprod))*100, order=c(1, 0, 1))

arma2_1<-Arima(diff(log(data$indprod))*100, order=c(2, 0, 1))

arma1_2<-Arima(diff(log(data$indprod))*100, order=c(1, 0, 2))

arma2_2<-Arima(diff(log(data$indprod))*100, order=c(2, 0, 2))

name<-c('AR(4)', 'MA(3)', 'ARMA(1,1)', 'ARMA(2,1)', 'ARMA(1,2)', 'ARMA(2,2)')

aic<-c(

AIC(ar4)/length(data$indprod),

AIC(ma3)/length(data$indprod),

AIC(arma1_1)/length(data$indprod),

AIC(arma2_1)/length(data$indprod),

AIC(arma1_2)/length(data$indprod),

AIC(arma2_2)/length(data$indprod)

)

bic<-c(

BIC(ar4)/length(data$indprod),

BIC(ma3)/length(data$indprod),

BIC(arma1_1)/length(data$indprod),

BIC(arma2_1)/length(data$indprod),

BIC(arma1_2)/length(data$indprod),

BIC(arma2_2)/length(data$indprod)

)

out<-data.frame(matrix(aic, nrow=1))

out<-rbind(out, bic)

colnames(out)<-name

rownames(out)<-c('AIC', 'SIC')

out

AR(4) MA(3) ARMA(1,1) ARMA(2,1) ARMA(1,2) ARMA(2,2)

AIC 3.232032 3.239599 3.324956 3.277746 3.233284 3.246579

SIC 3.296225 3.293094 3.367752 3.331241 3.286779 3.310772

## figure

par(mfrow = c(2, 2))

par(mar = c(2, 2, 1, 1))

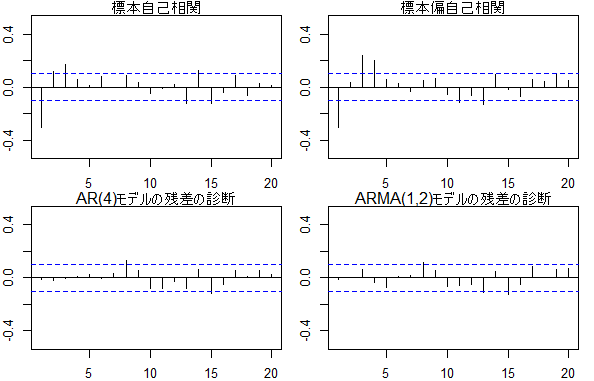

acf(diff(log(data$indprod)), xlim=c(1, 20), ylim=c(-0.5, 0.5))

mtext(text = '標本自己相関', side = 3)

pacf(diff(log(data$indprod)), xlim=c(1, 20), ylim=c(-0.5, 0.5))

mtext(text = '標本偏自己相関')

acf(ar4$residuals, xlim=c(1, 20), ylim=c(-0.5, 0.5))

mtext(text = 'AR(4)モデルの残差の診断', side = 3)

acf(arma1_2$residuals, xlim=c(1, 20), ylim=c(-0.5, 0.5))

mtext(text = 'ARMA(1,2)モデルの残差の診断', side = 3)

- (2)

library(forecast)

data<-read.table("economicdata.txt",header=T)

ar4<-Arima(diff(log(data$indprod))*100, order=c(4, 0, 0))

arma1_2<-Arima(diff(log(data$indprod))*100, order=c(1, 0, 2))

AR(4)

Box.test(ar4$residuals[1:10], type="Ljung")

Box-Ljung test

data: ar4$residuals[1:10]

X-squared = 0.37762, df = 1, p-value = 0.5389

p>0.05より帰無仮説を棄却できないので自己相関があるとは言えない。

ARMA(1, 2)

Box.test(arma1_2$residuals[1:10], type="Ljung")

Box-Ljung test

data: arma1_2$residuals[1:10]

X-squared = 0.37971, df = 1, p-value = 0.5378

p>0.05より帰無仮説を棄却できないので自己相関があるとは言えない。

2.6

library(forecast)

data<-read.table("arma.txt", header=T)

- (1)

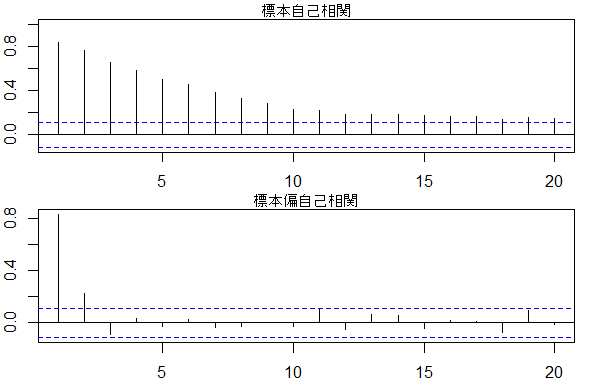

par(mfrow=c(2, 1))

acf(data$y1, xlim=c(1, 20))

mtext('標本自己相関', side = 3)

pacf(data$y1, xlim=c(1, 20))

mtext('標本偏自己相関', side = 3)

- (2), (3)

###AR(2)

###ARMA(1,1),ARMA(2,1),ARMA(1,2),ARMA(2,2)

ar2<-Arima(data$y1, order=c(2, 0, 0))

arma1_1<-Arima(data$y1, order=c(1, 0, 1))

arma2_1<-Arima(data$y1, order=c(2, 0, 1))

arma1_2<-Arima(data$y1, order=c(1, 0, 2))

arma2_2<-Arima(data$y1, order=c(2, 0, 2))

name<-c('AR(2)', 'ARMA(1,1)', 'ARMA(2,1)', 'ARMA(1,2)', 'ARMA(2,2)')

aic<-c(

AIC(ar2)/length(data$y1),

AIC(arma1_1)/length(data$y1),

AIC(arma2_1)/length(data$y1),

AIC(arma1_2)/length(data$y1),

AIC(arma2_2)/length(data$y1)

)

bic<-c(

BIC(ar2)/length(data$y1),

BIC(arma1_1)/length(data$y1),

BIC(arma2_1)/length(data$y1),

BIC(arma1_2)/length(data$y1),

BIC(arma2_2)/length(data$y1)

)

out<-data.frame(matrix(aic, nrow=1))

out<-rbind(out, bic)

colnames(out)<-name

rownames(out)<-c('AIC', 'SIC')

###AIC ARMA(2,1), SIC AR(2)

out

AR(2) ARMA(1,1) ARMA(2,1) ARMA(1,2) ARMA(2,2)

AIC 3.023947 3.034293 3.021437 3.029152 3.027627

SIC 3.073331 3.083677 3.083167 3.090882 3.101703

- (4)

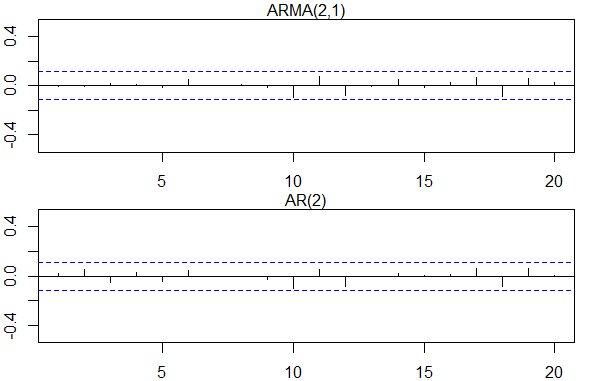

AICからはARMA(2,1)、SICからはAR(2)を選択した。

acf(arma2_1$residuals, xlim=c(1,20), ylim=c(-0.5,0.5))

acf(ar2$residuals, xlim=c(1,20), ylim=c(-0.5,0.5))

Box.test(arma2_1$residuals[1:20], type="Ljung")

Box-Ljung test

data: arma2_1$residuals[1:20]

X-squared = 0.013201, df = 1, p-value = 0.9085

Box.test(ar2$residuals[1:20], type="Ljung")

Box-Ljung test

data: ar2$residuals[1:20]

X-squared = 0.0979, df = 1, p-value = 0.7544

- (5)

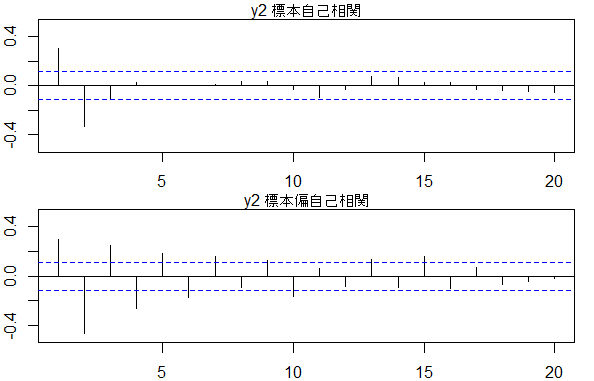

y2

acf(data$y2, xlim = c(1, 20), ylim = c(-0.5, 0.5))

mtext(text = 'y2 標本自己相関', side = 3)

pacf(data$y2, xlim = c(1, 20), ylim = c(-0.5, 0.5))

mtext(text = 'y2 標本偏自己相関', side = 3)

####MA(3)

####ARMA(1,1),ARMA(2,1),ARMA(1,2),ARMA(2,2)

ma3<-Arima(data$y2, order=c(0, 0, 3))

arma1_1<-Arima(data$y2, order=c(1, 0, 1))

arma2_1<-Arima(data$y2, order=c(2, 0, 1))

arma1_2<-Arima(data$y2, order=c(1, 0, 2))

arma2_2<-Arima(data$y2, order=c(2, 0, 2))

name<-c('MA(3)', 'ARMA(1,1)', 'ARMA(2,1)', 'ARMA(1,2)', 'ARMA(2,2)')

aic<-c(

AIC(ma3)/length(data$y2),

AIC(arma1_1)/length(data$y2),

AIC(arma2_1)/length(data$y2),

AIC(arma1_2)/length(data$y2),

AIC(arma2_2)/length(data$y2)

)

bic<-c(

BIC(ma3)/length(data$y2),

BIC(arma1_1)/length(data$y2),

BIC(arma2_1)/length(data$y2),

BIC(arma1_2)/length(data$y2),

BIC(arma2_2)/length(data$y2)

)

out<-data.frame(matrix(aic, nrow=1))

out<-rbind(out, bic)

colnames(out)<-name

rownames(out)<-c('AIC', 'SIC')

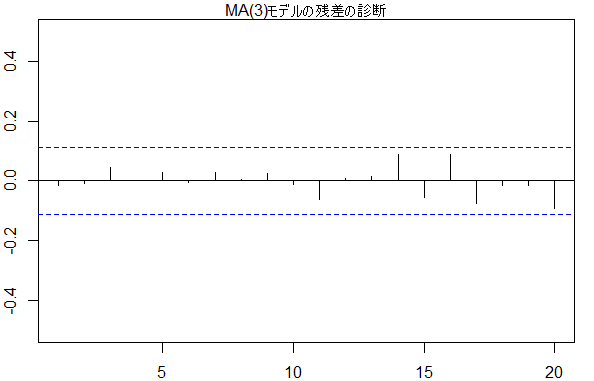

###AIC MA(3), SIC MA(3)

out

MA(3) ARMA(1,1) ARMA(2,1) ARMA(1,2) ARMA(2,2)

AIC 2.769046 2.859515 2.775498 2.818165 2.781784

SIC 2.830775 2.908899 2.837228 2.879895 2.855860

par(mfrow = c(1, 1))

acf(ma3$residuals, xlim=c(1,20), ylim=c(-0.5,0.5))

Box.test(ma3$residuals[1:20], type="Ljung")

Box-Ljung test

data: ma3$residuals[1:20]

X-squared = 0.0066437, df = 1, p-value = 0.935

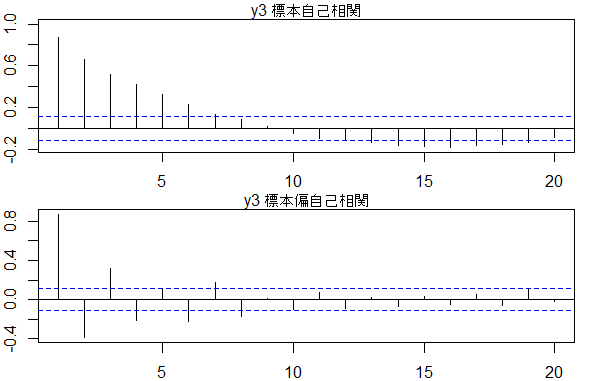

y3

###y3

par(mfrow=c(2,1))

acf(data$y3, xlim=c(1, 20))

mtext(text = 'y3 標本自己相関', side = 3)

pacf(data$y3, xlim=c(1, 20))

mtext(text = 'y3 標本偏自己相関', side = 3)

####AR(8), MA(7)

####ARMA(1,1),ARMA(2,1),ARMA(1,2),ARMA(2,2)

ar8<-Arima(data$y3, order=c(8, 0, 0))

ma7<-Arima(data$y3, order=c(0, 0, 7))

arma1_1<-Arima(data$y3, order=c(1, 0, 1))

arma2_1<-Arima(data$y3, order=c(2, 0, 1))

arma1_2<-Arima(data$y3, order=c(1, 0, 2))

arma2_2<-Arima(data$y3, order=c(2, 0, 2))

name<-c('AR(8)', 'MA(7)', 'ARMA(1,1)', 'ARMA(2,1)', 'ARMA(1,2)', 'ARMA(2,2)')

aic<-c(

AIC(ar8)/length(data$y3),

AIC(ma7)/length(data$y3),

AIC(arma1_1)/length(data$y3),

AIC(arma2_1)/length(data$y3),

AIC(arma1_2)/length(data$y3),

AIC(arma2_2)/length(data$y3)

)

bic<-c(

BIC(ar8)/length(data$y3),

BIC(ma7)/length(data$y3),

BIC(arma1_1)/length(data$y3),

BIC(arma2_1)/length(data$y3),

BIC(arma1_2)/length(data$y3),

BIC(arma2_2)/length(data$y3)

)

out<-data.frame(matrix(aic, nrow=1))

out<-rbind(out, bic)

colnames(out)<-name

rownames(out)<-c('AIC', 'SIC')

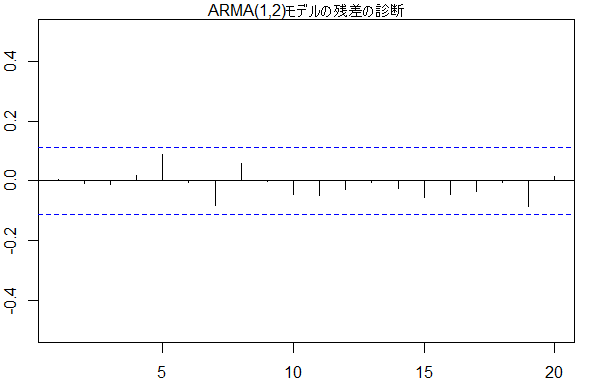

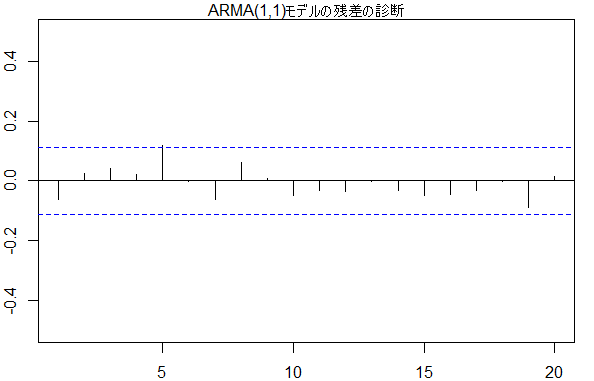

###AIC ARMA(1,2), SIC ARMA(1,1)

out

AR(8) MA(7) ARMA(1,1) ARMA(2,1) ARMA(1,2) ARMA(2,2)

AIC 3.115248 3.082550 3.069798 3.06590 3.065178 3.071635

SIC 3.238708 3.193663 3.119182 3.12763 3.126907 3.145711

par(mfrow = c(1, 1))

acf(arma1_2$residuals, xlim=c(1,20), ylim=c(-0.5,0.5))

mtext(text = 'ARMA(1,2)モデルの残差の診断', side = 3)

Box.test(arma1_2$residuals[1:20], type="Ljung")

Box-Ljung test

data: arma1_2$residuals[1:20]

X-squared = 0.17219, df = 1, p-value = 0.6782

acf(arma1_1$residuals, xlim=c(1,20), ylim=c(-0.5,0.5))

mtext(text = 'ARMA(1,1)モデルの残差の診断', side = 3)

Box.test(arma1_1$residuals[1:20], type="Ljung")

Box-Ljung test

data: arma1_1$residuals[1:20]

X-squared = 6.0017e-05, df = 1, p-value = 0.9938

⇒ 3章はプログラムを用いる章末問題がないので、次は 『経済・ファイナンスデータの計量時系列分析』章末問題をRで解く-第4章VARモデル- へ