今まで時系列のplotはしても分析らしい分析に触れる機会がなかったが、セミナーで習ったことを振り返りついでになぞる。

原理の部分は次回

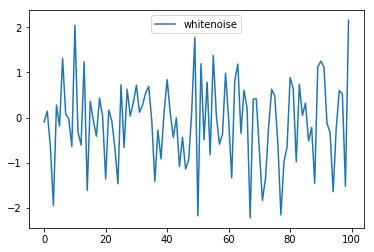

ホワイトノイズ(不規則なノイズ)の生成

import pandas as pd

import numpy as np

from matplotlib import pyplot as plt

%matplotlib inline

import statsmodels.api as sm

a = np.random.normal(0, 1, 100)

df_whitenoise = pd.DataFrame(a, columns = ["whitenoise"])

df_whitenoise.head()

df_whitenoise.plot()

whitenoise

0 -0.096781

1 0.140867

2 -0.624550

3 -1.946654

4 0.274500

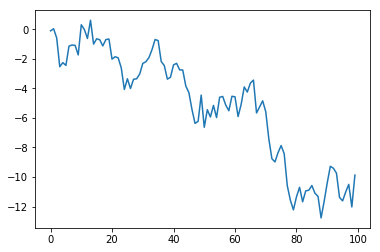

ランダムウォークの生成

ホワイトノイズの値の累積和(前回の値と足し算)することで、ランダムな時系列変化があるようなグラフを作る

df_randomwalk = df_whitenoise.assign(whitenoise = np.cumsum(df_whitenoise.whitenoise))

plt.plot(df_randomwalk)

下がっていくような傾向があるように見えるが、実際は無意味に動いているだけ。

投資などの予想が難しいのはこのため。

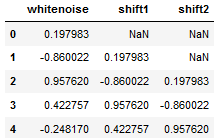

値をズラすshift(periods=1)

値をズラしたデータを作ることで自己相関の計算がしやすくなる。

df_whitenoise["shift1"] = df_whitenoise["whitenoise"].shift(periods=1)

df_whitenoise["shift2"] = df_whitenoise["whitenoise"].shift(periods=2)

df_whitenoise.head()

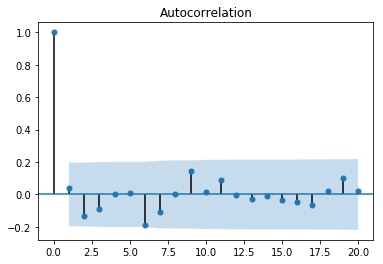

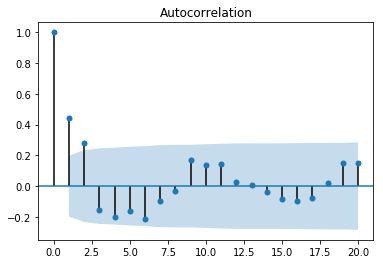

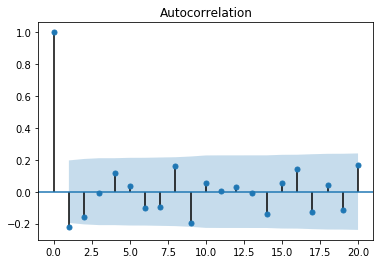

自己相関を見るACF

自己相関関数は、k時間単位離れた時系列の観測値間の相関(ytとyt-k)を表す

sm.graphics.tsa.plot_acf(df_whitenoise.whitenoise, alpha=0.05,lags=20)

最初のスパイクが優位に検知されている。

その後のスパイクは有意水準95%の範囲内に収まっている。

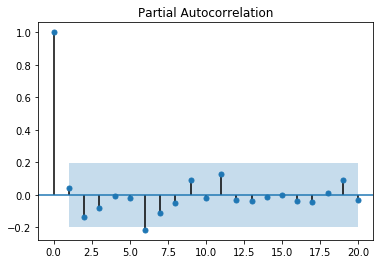

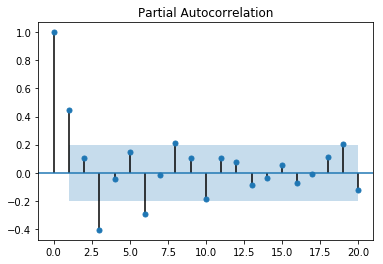

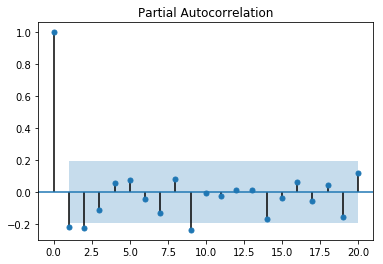

偏自己相関PCAF

偏自己相関関数は、遅れが短いその他のすべての項(yt-1、yt-2、...、yt-k-1)の存在を考慮して調整した後に計算される、k時間単位離れた時系列の観測値間の相関(ytとyt-k)を表す

sm.graphics.tsa.plot_pacf(df_whitenoise.whitenoise, alpha=0.05,lags=20)

移動平均過程 MA

時系列はすべての時刻で同じ分布からデータが出てくるわけではない。

時刻が異なれば、分布も異なる。

過去の値を加えていくことで現在の分布を表している。

df_whitenoise["ma"] = df_whitenoise["whitenoise"] + df_whitenoise["shift1"]*0.5 + df_whitenoise["shift2"]*0.8 + 1

df_whitenoise = df_whitenoise.dropna()

plt.plot(df_whitenoise[["ma"]])

sm.graphics.tsa.plot_acf(df_whitenoise[["ma"]], lags=20)

sm.graphics.tsa.plot_pacf(df_whitenoise[["ma"]], lags=20)

自己回帰過程 AR

過去のデータから影響を受ける。

定数部は確定できない影響を説明している。

df_whitenoise["ar"] = 0

df_whitenoise["shift1"] = 0

df_whitenoise["shift2"] = 0

for i in range(100):

df_whitenoise.iloc[i, 1] = df_whitenoise.iloc[i, 0] + 0.8*df_whitenoise.iloc[i, 2] + 0.3*df_whitenoise.iloc[i, 3] + 2

df_whitenoise.iloc[i, 2] = df_whitenoise.iloc[i-1, 1]

df_whitenoise.iloc[i, 3] = df_whitenoise.iloc[i-2, 1]

plt.plot(df_whitenoise[["ar"]])

sm.graphics.tsa.plot_acf(df_whitenoise[["ar"]], lags=20)

sm.graphics.tsa.plot_pacf(df_whitenoise[["ar"]], lags=20)

ACF

PACF

#UKgasで時系列予想

(同志社大のデータサイエンス研究室のHPでRでおなじようなことをやっている)

UKgasはRからcsvを作っておく

gas_csv <- data.frame(UKgas)

year <- seq(1960,1986,1)

mon <- c(1,4,7,10)

day <- c(1)

limit <- (nrow(gas_csv)/4)

time <- NULL

for (i in 1:limit){

N1<- paste0(year[i],"/",mon[1],"/",day)

N2<- paste0(year[i],"/",mon[2],"/",day)

N3<- paste0(year[i],"/",mon[3],"/",day)

N4<- paste0(year[i],"/",mon[4],"/",day)

time <- c(time,N1,N2,N3,N4)

}

write.csv(data.frame(time=time, UKgas=gas_csv), "UKgas.csv" ,row.names=F)

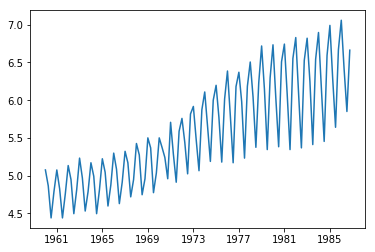

パイソンに戻る

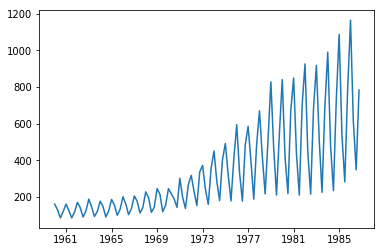

とりあえずプロット

df = pd.read_csv("UKgas.csv", index_col=0)

df.index = pd.to_datetime(df.index)

plt.plot(df)

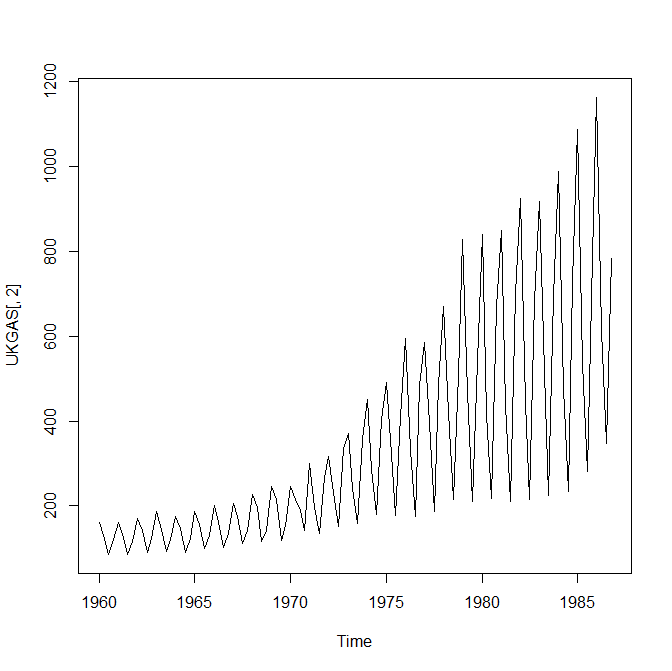

Rでやるならこんな感じ

UKGAS <- data.frame(time=time, UKgas=gas_csv)

ts.plot(UKGAS[,2])

ガスは四半期で周期的に動いているのがわかる(ギザギザしている)

冬は消費量が多く夏は少ない。

増え方も大きい。

対数をとって差分(足し引き)のカタチにしてわかりやすくする。

df["UKgas"] = np.log(df["UKgas"])

plt.plot(df)

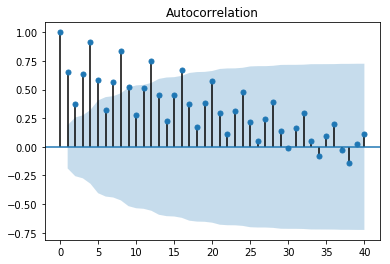

sm.graphics.tsa.plot_acf(df, lags=40)

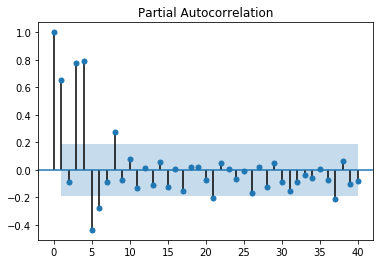

sm.graphics.tsa.plot_pacf(df, lags=40)

ACF

四半期の周期性がわかる

PACF

最初の方のスパイクが反応している

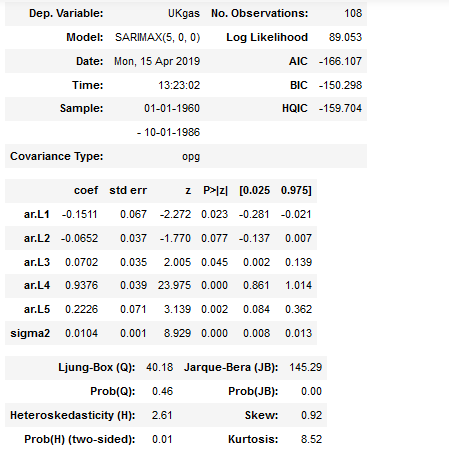

fit = sm.tsa.SARIMAX(df, order=(5,0,0), seasonal_order=(0,0,0,4),

enforce_invertibility=False,

enforce_stationarity=False).fit()

fit.summary()

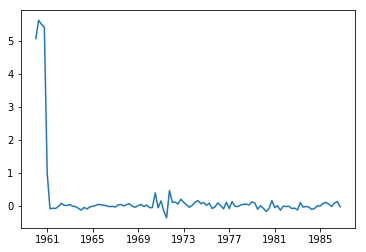

plt.plot(fit.resid)

SARIMAXを調整してAICやBICが小さくなるようなモデルを見つける。

誤差を見ると最初は反応しているが、あとは小さい値。

1969~1977年に誤差が発生している

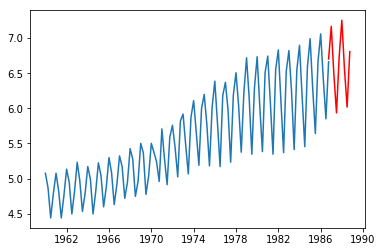

predictで予想値を二年分出す

pred = fit.predict('1986-10-01', '1988-10-01')

plt.plot(df)

plt.plot(pred, "r")

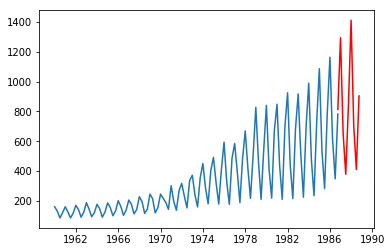

対数処理をnp.expで戻す

予測値が見えました。

上昇傾向にありそうです。

周期性も再現できていそうです。