上値抵抗性突破とは

過去N日間の株価終値の最高値を、今日の終値が突破した時、さらに上昇することを期待して買いポジションを持つストラテジーです。

とても簡単なアルゴリズムなので、コードも簡単に書けます。

シグナル

過去90日間の終値の最高値を今日の終値が突破した場合、ロングポジションを持つ。

手仕舞い

益出し:+5%

損切り:ー3%

コード

(昨日の勉強会で知ったのですが、QuantXのコードは公開+Cloneできるんですね。ログイン後、このリンクを辿って、上にあるクローンボタンをおしてクローンしてください。)

clone : https://factory.quantx.io/developer/2729d13d204b4f2db1c08385ad5d13b0

############################################################################

# 上値抵抗線突破

############################################################################

def initialize(ctx):

ctx.target = 0.10

ctx.period = 90

ctx.loss_cut = -0.03

ctx.plofit = 0.05

ctx.codes = [1605, 1925, 2503, 4519, 4911, 6301, 6752, 7741, 8001 ]

ctx.symbol_list = ["jp.stock.{}".format(code) for code in ctx.codes]

ctx.configure(

channels={

"jp.stock": {

"symbols": ctx.symbol_list,

"columns": ["close_price_adj", # 終値(株式分割調整後)

]}})

def _RESISTANCE_LINE(data):

df_close = data["close_price_adj"].fillna(method='ffill')

df_Max_close = df_close.rolling(window=ctx.period).max()

buy_sig = df_Max_close == df_close

# memo 参照

ctx.logger.info(df_Max_close.tail())

return {

"buy:sig": buy_sig,

"max": df_Max_close,

}

# シグナル登録

ctx.regist_signal("RESISTANCE_LINE", _RESISTANCE_LINE)

def handle_signals(ctx, date, current):

# ポジションクローズ

for (sym,val) in ctx.portfolio.positions.items():

rtn = val["returns"]

if rtn < ctx.loss_cut:

sec = ctx.getSecurity(sym)

# memo 参照

sec.order_target_percent(0, comment="損切り {:.2%}".format(rtn))

elif rtn > ctx.plofit:

sec = ctx.getSecurity(sym)

sec.order_target_percent(0, comment="益出し {:.2%}".format(rtn))

df = current.copy()

df = df[df["buy:sig"]]

if not df.empty:

for (sym, val) in df.iterrows():

sec = ctx.getSecurity(sym)

sec.order_target_percent(ctx.target, comment= "シグナル買")

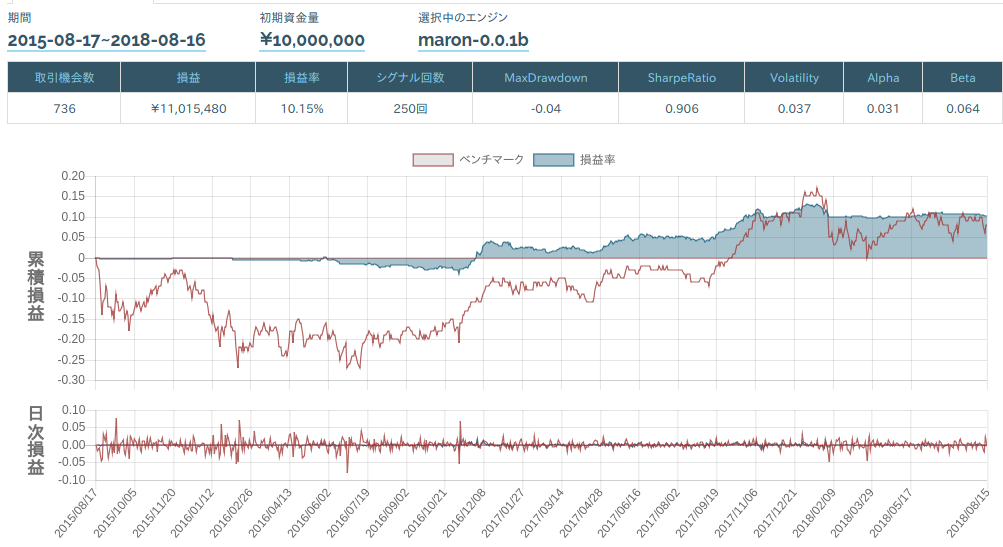

結果

memo

log と print

QuantX では print は使用不可です。

出力したい場合は、ctx.logger.info (レベルは debut/info/warn/error/critical ) が使えます。

ログは、IDE画面の下に出るログ画面に表示されます。

order_target_percent の comment

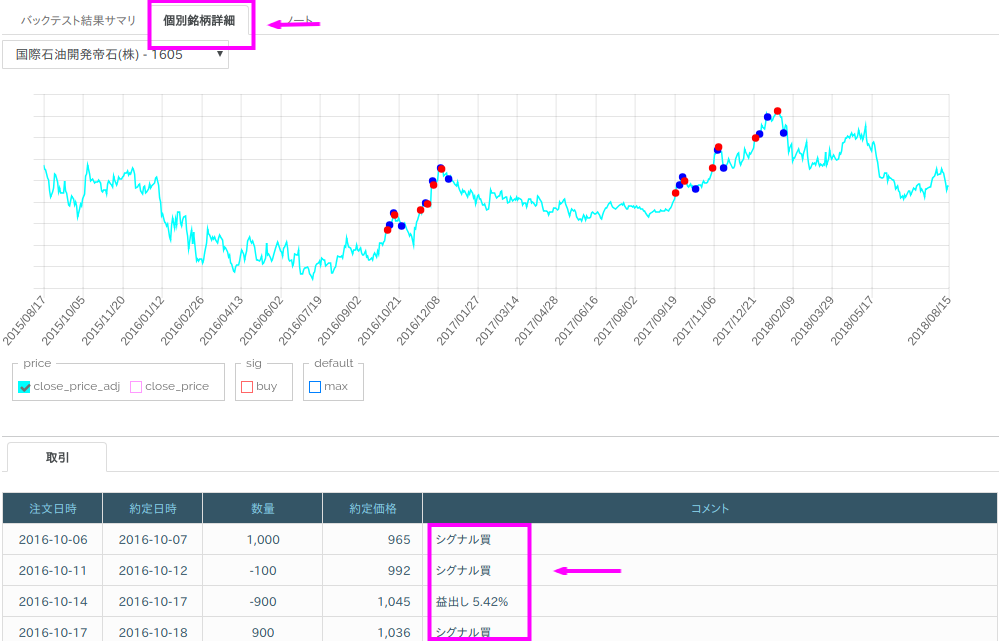

上のコードの sec.order_target_percent(0, comment="損切り {:.2%}".format(rtn))で使っているcomment はどこに出力されるの?という質問を受けました。

バックテストの結果画面の、個別銘柄詳細タブを開くと、各個別銘柄の各取引を確認できます。そこにコメントという欄がありそこで確認できます。

感想

QuantX ユーザーのための pandas 勉強会をしたほうがいいなーと思っています。

免責注意事項

- このコードに基づき投資した結果、損害が発生しても,一切責任を持ちません.

- このコードが正しく機能する保証は一切致しません.

- このアルゴリズムを勧めているわけではありません.あくまで QuantX / Python のサンプルコードとして掲載しているだけです.