本記事の目的は、金融経済学の授業で学んだことの復習になります。CS分野に直接は関係ないのですが、間接的に役に立つこともあるやもしれませんので、公開させて頂きます。しかしあくまで授業の復習なので、定義についてなどそこまで細かく言及することはしていません。

また、私自身経済学もあまり馴染みはないので、訂正依頼などあれば気軽に教えてください。

The purpose of this article is to review the sessions of Financial Economics. Actually, even though it doesn't seem to be related to Computer Science field directly, I open this to the public because it might be helpful to understand Financial Economics x CS field, for instance in the situation that you want to analyze stock trading with Deep Learning.

1. 金融資産 / Financial Assets

この章ではまず、金融経済学の導入として金融資産の定義を行います。そしてその後、金融資産をその定義に基づいてカテゴリー分類していき、それぞれについての説明を行います。

On this chapter, first of all, I offer the definition of "what is financial assets". Then, I categorize some financial assets into fine pieces based on the definition and explain the details for each.

1.1. 金融資産とは / Definition of financial assets

そもそも、資産とは何なのでしょうか。資産とは、財産権が明確に定義された価値のあるものだと授業では習いました。例えば、100スイスフランの紙幣、ヤギ(スイスならではの例)、ローン、保険契約などが挙げられます。

そして金融資産はそれに対し、元来価値は備わっていないが、ある特定の出来事に付随して義務や権利が発生し価値を持つようになるものだと一般的には考えられているようです。例えば、金銭契約や株、オプションなどが挙げられます。

しかし、金融資産と非金融資産の定義は曖昧で、明確な線引きはされていないようです。(なんやねん笑)

In the first place, what is "ASSETS"?

Assets is thought as something valuable with well-defined property right, for example a 100CHF banknote, a goat (Swiss example), a loan, an insurance contract.

On the other hand, Financial Assets is thought as something that has no intrinsic value usually, however has values and comes with rights or obligations in the future, which may be contingent on the realization of specific events. For example, bonds, stocks, options, annuities and so on.

However, the distinction between financial assets and non-financial assets is not clear.

1.2. 金融資産の分類 / Categorizing financial assets

では、金融資産の簡易的な定義を行ったところで、金融資産を二つに分類していきます。

Then, after supplying a definition for financial assets, let's categorize financial assets into two.

安全資産(Riskless assets):

確実性を持って将来価値が保証されている資産(例:国債、現金、預貯金)

Assets whose future values can be known with uncertainty (e.g. federal bond, cash, deposit)

危険資産(Risky assets):

将来価値がなんらかの出来事に左右され得る資産(例:保険契約、株、オプション)

Assets whose future values may depend on the realization of some events (e.g. health insurance, stocks, options)

2. 安全資産 / Riskless Assets

厳密に言えば、不履行の可能性は常に存在するので、真にリスクのない安全資産というものは存在しません。安全資産とは、単に理論的なものに過ぎないのです。

しかしながら、以下に挙げるようなものは安全資産だと一般的には考えられています。

・政府によって発行されている国債

・銀行によって保証されている貯蓄

・金融政策によって普及している紙幣

重要なことは、安全かどうかというのはその資産がどの機関によって管理されているかに依存するということです。

As the risk of default always exists, there are, strictly speaking, no pure riskless assets. Riskless assets are purely theoretical.

However, the following items are considered (almost) riskless assets.

・Government bonds depending on the country

・Savings accounts depending on the bank

・Banknotes depending on the monetary policy

Remark that the notion of "safe" depends on the unit of reference.

2.1. ゼロクーポン債(割引債) / Zero-coupon bond

安全資産の一つに、ゼロクーポン債というものがあります。

ゼロクーポン債とは、利子の支払いがなく、満期までの利子に相当する金額をあらかじめ債券の額面金額から差し引いた価格で発行され、満期時に額面金額で償還される債券のことを指します。

厳密にはゼロクーポン債は海外の割引債のことを指すようですが、ここでは割引債と同義だとします。

Zero-coupon bond is one of the riskless assets.

A zero-coupon bond is a debt security that doesn't pay interest (a coupon) but is traded at a deep discount, rendering profit at maturity when the bond is redeemed for its full face value.

2.2. ディスカウンティング / Discounting

ディスカウンティングとは、将来の価値を現在価値に置き換えるプロセスです。時点$t$における価値を$x_t$,割引率を$r_t$としたとき、$x_t$の現在価値そして時点Tまでの総和現在価値は以下の式で表されます。

Discounting is the process of determining the present value (i.e. at time $t=0$) of a future payment $x_t$ at time $t>0$. When $x_t$ is defined as the value at time $t$ and $r_t$ is defined as the discount rate at time $t$, we can see the formula representing the present value of $x_t$ and sum of the present values till time $T$ as follows.

離散時間 (discrete time):$$PV(x_t)=\frac{x_t}{\prod_{i=0}^{t-1}(1+r_i)}$$

$$PV(x)=\sum_{t=0}^TPV(x_t)=\sum_{t=0}^T\frac{x_t}{\prod_{i=0}^{t-1}(1+r_i)}$$

連続時間 (continuous time):$$PV(x_t)=e^{-\int_{0}^tr(\tau)d\tau}x_tdt$$

$$PV(x)=\int_{0}^TPV(x_t)=\int_{0}^Te^{-\int_{0}^tr(\tau)d\tau}x_tdt$$

2.3. コンパウンディング / Compounding

コンパウンディングとは、現在の価値を将来価値に置き換えるプロセスです。時点$t$における価値を$x_t$,割引率を$r_t$としたとき、$x_0$の将来価値は以下の式で表されます。

Compounding is the process of determining the value at time $t$ (in the future) of monetary amount $x_0$ invested at time $t=0$. When $x_t$ is defined as the value at time $t$ and $r_t$ is defined as the interest rate at time $t$, we can see the formula representing the future value of $x_0$ as follows.

離散時間 (discrete time):$$CV_t(x_0)=\prod_{i=0}^{t-1}(1+r_i)x_0$$

2.4. 割引率 / Discount rates

割引率に基づいてディスカウンティングやコンパウンディングを行う際、その割引率の用い方は二種類あります。

When we implement discounting or compounding with discount rates, there are two options to adopt. On this part, discount rates is equivalent to interest rates.

スポット・レート / Spot interest rates

スポット・レートは、現在から一定期間後に満期となる割引債の利回り(複利利回り)のことです。このスポット・レートを用いることによって、ゼロクーポン債の債券価格をより現実的に求めることが可能になります。

例えば、満期までの期間が3年,クーポン・レート5%,額面100円のゼロクーポン債の債券価格は、以下のようになります。

Spot interest rates correspond to the interest rates offered today (time $t=0$) on zero-coupon bonds of varying maturities $t>0$. With utilizing Spot interest rates, it enables us to calculate the present value of zero coupon bond more realistic.

For instance, when we put the maturity $t=3 years$, coupon rate $c=5$% and face amount $p=100yen$,

the present value of zero coupon bond will be calculated as follows.

$$PV=\frac{5}{1+r_1}+\frac{5}{(1+r_2)^2}+\frac{5+100}{(1+r_3)^3}$$

そしてこのとき、

1年物スポット・レート $r_1=6$%

2年物スポット・レート $r_2=7$%

3年物スポット・レート $r_3=8$%

とすれば、額面100円のゼロクーポン債の現在価値は以下となります。

Then, when we put

spot interest rates for 1 year $r_1=6$%

spot interest rates for 2 years $r_2=7$%

spot interest rates for 3 years $r_3=8$%,

the present value of zero coupon

with face amount $p=100yen$ will be following amount.

$$PV=\frac{5}{1+0.06}+\frac{5}{(1+0.07)^2}+\frac{5+100}{(1+0.08)^3}=92.436yen$$

フォワード・レート / Forward interest rates

フォワード・レートとは、将来のある時点から、さらに先のある時点までの間の期間の利率のことを指します。市場取引に裁定が働くことを前提にすれば、現時点でのスポット・レートの体系から将来の金利予測を行うことが可能になります。しかし、現在のレートに基づいて予測を行うだけなので、将来そのレートが実現することは全く保証されていません。

ここで、一年後から二年後までのフォワード・レートを${f_{1,2}}$とすれば、先ほどの変数を用いて${f_{1,2}}$は以下のように表されます。

Forward interest rates correspond to the anticipated spot rates at future dates. Assumed that arbitrage will be worked towards the market trading, we will be able to anticipate the future interest rates based on spot interest rates at the moment. However, it is never guaranteed to realize the forward interest rates because it is only anticipated with the current rates, which means that it's just the theoretical rates.

When we put

spot interest rates for 1 year: $r_1$

spot interest rates for 2 years: $r_2$

forward interest rates from the 1st year to 2nd year: ${f_{1,2}}$,

$$1+{f_{1,2}}=\frac{(1+{r_2})^2}{1+r_1}$$

イールド・カーブ / Yield curve

スポット・レートは満期までの期間の長さ(残存期間)によって利回りが異なります。

イールド・カーブ(利回り曲線)は、横軸に満期までの期間、縦軸に利回りをとって、割引債の残存期間と利回りとの関係をグラフで表したものです。

Spot interest rates depends on the remaining duration of maturity.

Yield curve shows the relationship between the remaining duration and the interest rates in a graph with remaining duration on horizontal line and rates on vertical line.

3. 危険資産 / Risky Assets

危険資産は、金融資産の中でも将来価値がなんらかの出来事に左右され得る資産を指します。例えば、以下のようなものが危険資産に当たります。

・株

・デリバティブ(金融派生商品)

・保険契約

Risky assets are the assets whose future values may depend on the realization of some events.

e.g. )

・Stocks:assets whose value is related to the performance of the firms and to the "mood of the market" (expectations of other agents)

・Derivatives

・Health insurance

3.1. デリバティブ / Derivatives

デリバティブとは、その資産価値が他の金融商品に依存する資産です。金融派生商品とも呼ばれます。デリバティブには、以下のような種類があります。

Derivatives are assets whose values mechanically depend on the values of other financial assets like the following examples.

先物取引 / Futures contract

将来の売買について、予め現時点で約束する取引のことをいいます。この取引は、ある対象商品を将来の一定の期日に、今の時点で取り決めた価格で取引することを約束(保証)する契約であり、それは義務となります。

対象商品には、コモディティ商品や株、通貨そして利率などの無形資産があります。

Futures contract is the contract that makes a promise about future trading. Future contract has the obligation to purchase (long position) or sell (short position) the underlying at a specified future price at a specified delivery date.

The underlying may be a commodity (wheat, iron,...), a stock, a currency or an intangible such as an interest rate.

オプション取引 / Option contract

オプション取引とは、ある商品について、将来の一定の期日(期間内)に一定の数量を、その時の市場価格に関係なく予め決められた特定の価格(権利行使価格)で買う権利または売る権利を売買する取引のことです。

オプションの売り手はショートポジションを取り、オプションの買い手はロングポジションを取ります。

対象商品には、先物取引と同じようなコモディティ商品や株、通貨そして利率などの無形資産があります。

Option contract has the right to purchase (call option) or sell (short position) a specified amount of the underlying at a specified 'exercise price' at or before a specified expiration date.

The writer of the position has a short position and the owner of the option has a long position.

The underlying may be a commodity (wheat, iron,...), a stock, a currency or an intangible such as an interest rate as like the same case of futures contract.

先物取引とオプション取引の大きな違いは、その取引の行使が義務か権利かということです。それでは次に、このようなデリバティブにはどのような機能があるのか見ていきましょう。

The big difference between them is whether the transaction is the obligation or the right. Then, let's see the functions of those derivatives.

ヘッジング / Hedging

ヘッジングとは、対象商品の価値変動リスクを回避・軽減することです。デリバティブを所有することによって、価格変動によらないリターンを得ることができます。

Hedging is an action to insure against market price volatility. By owning derivatives, a farmer receives a certain return fir his products.

投機 / Speculation

投機とは、対象商品の価値変動による利益を得ることを目的に売買を行うことです。デリバティブは少ない投資金額で取引が可能なので、その投資流動性が非常に高くなっています。(レバレッジ効果)

Speculation is an action to exploit profits from market price volatility.

Because derivatives can be traded with small amount of investment, it provides the speculators with many opportunities to speculate. (Leverage Effect)

3.2. オプション取引 / Options

既出になりますが、オプション取引とは、ある商品について、将来の一定の期日(期間内)に一定の数量を、その時の市場価格に関係なく予め決められた特定の価格(権利行使価格)で買う権利または売る権利を売買する取引のことです。オプションの売り手はショートポジションを取り、オプションの買い手はロングポジションを取ります。

対象商品には、先物取引と同じようなコモディティ商品や株、通貨そして利率などの無形資産があります。

オプション取引は、以下のようにそれぞれ分類されます。本記事では今後、ユーロピアンオプションを基本的には扱います。

Option contract has the right to purchase (call option) or sell (short position) a specified amount of the underlying at a specified 'exercise price' at or before a specified expiration date.The writer of the position has a short position and the owner of the option has a long position.

The underlying may be a commodity (wheat, iron,...), a stock, a currency or an intangible such as an interest rate as like the same case of futures contract.

Options is differed by as follows. On this article, basically we consider European rather than American options.

- ポジション / Position

- Long :option holder (right to exercise the option)

- Short:option writer (obligation to facilitate the option's exercise)

- 権利タイプ / Type of right

- Call:long position has the right to purchase an asset for $X$

- Put :long position has the right to sell an asset for $X$

- 期限前行使 / Possibility of early exercise

- American Option:exercise at or before expiration date $T$

- European Option:exercise at expiration date $T$

それでは、ポジションと権利タイプそれぞれの組み合わせについて説明していきましょう。説明の際、それぞれの変数を以下のように設定しています。また重要なこととして、購入されたオプションが行使されなかった場合、そのオプションの権利はoption writerに戻ります。

Then, let's see more details for each combinations of Position and Type of right. On each combination, we put the following variables.

・権利行使価格 / Exercise price of option:$X$

・$T$期(満期)における対象商品の市場価格 / market price of the underlying at expiration date $T$:$S_T$

・オプションの購入価格 / Purchase price of option:$Premium$

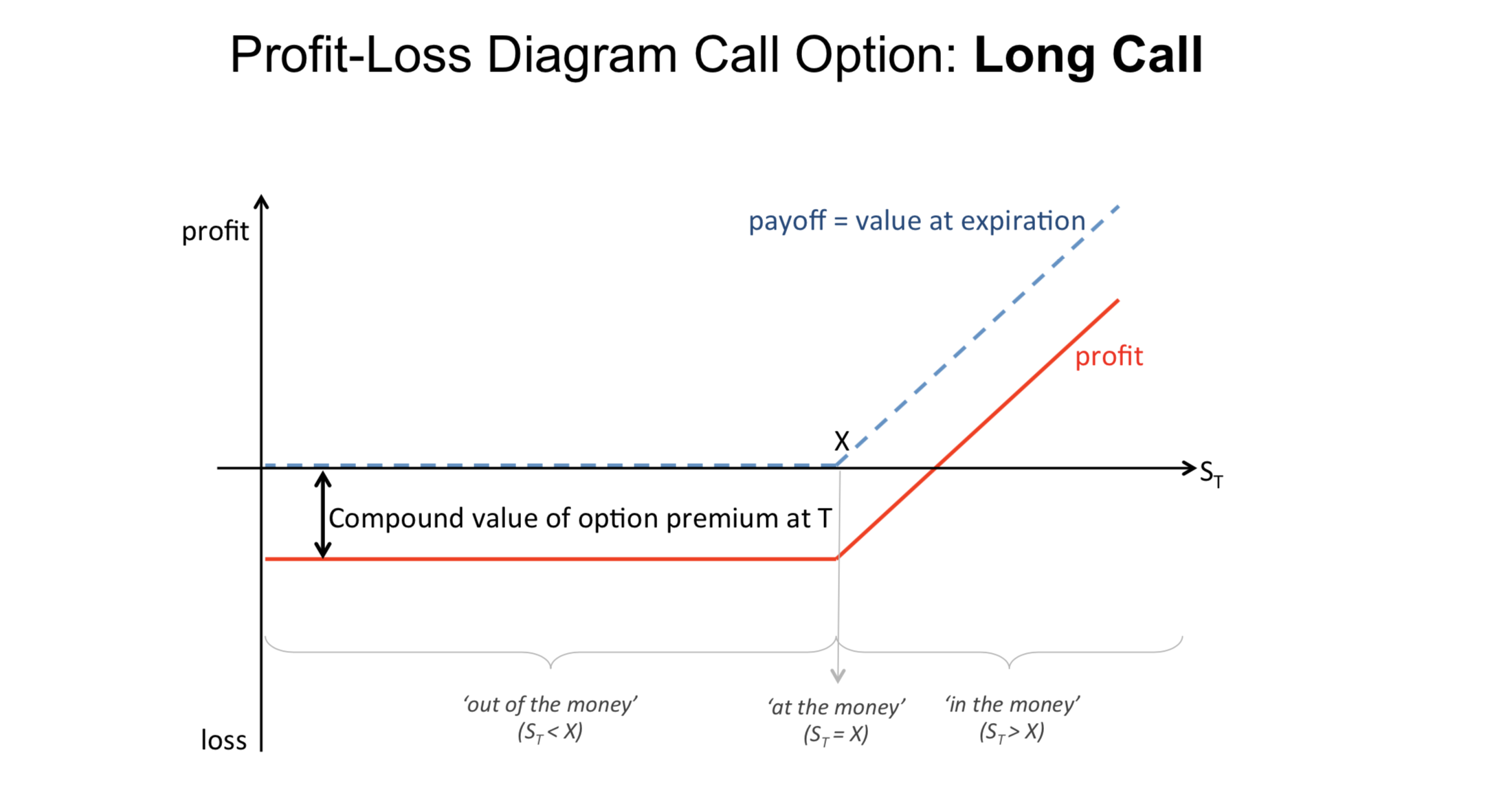

ロング・コール / Long Call

ロング・コールとは、オプション取引においてコール・オプションを買うことをいいます。また、コール・オプションとは、ある商品を将来のある一定期日(期間内)に、その時の市場価格に関係なく、予め決められた一定価格(権利行使価格)で購入することができる権利をいいます。

一般にロング・コールでは、期待通りに原資産の価格が上昇した場合は、売却時のプレミアムが上昇して利益(理論上無制限)となりますが、その一方で原資産の価格が権利行使価格まで上昇しなかった場合はその権利を行使しないため、損失は購入時のプレミアムに限定されます。

Long call is the most basic option to buy call options. Call options is the right to purchase a specified amount of the underlying at a specified 'exercise price' at or before a specified expiration date.

On long call, generally speaking, if the price of the underlying increases as expected, investors can get profit by increasing of the premium for selling. On the other hand, if the price of the underlying does not achieve the expected price, the financial loss is limited to the premium for purchasing.

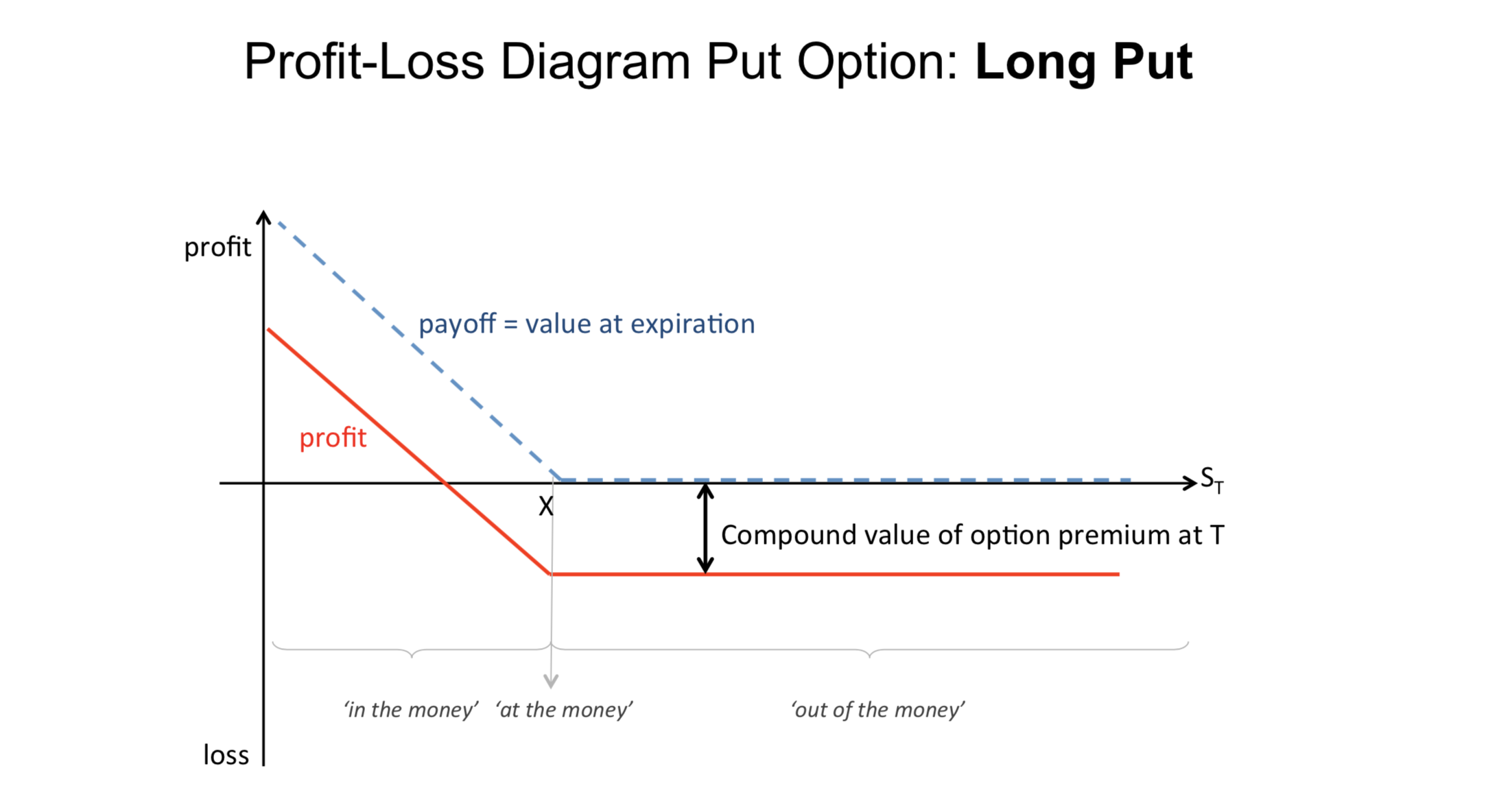

ロング・プット / Long Put

ロング・プットとは、オプション取引においてプット・オプションを買うことをいいます。また、プット・オプションとは、ある商品を将来のある一定期日(期間中)に、その時の市場価格に関係なく、予め決められた一定価格(権利行使価格)で売却することができる権利をいいます。

一般にロング・プットでは、期待通りに原資産の価格が下落した場合は、売却プレミアムが相対的に上昇して利益となりますが、その一方で原資産の価格が権利行使価格まで下落しなかった場合は、損失はプレミアムに限定されます。

Long put is the option to buy put options. Put options is the right to sell a specified amount of the underlying at a specified 'exercise price' at or before a specified expiration date.

On long put, generally speaking, if the price of the underlying decreases as expected, investors can get profit by increasing of the premium relatively for selling. On the other hand, if the price of the underlying does not achieve the expected price, the financial loss is limited to the premium for purchasing.

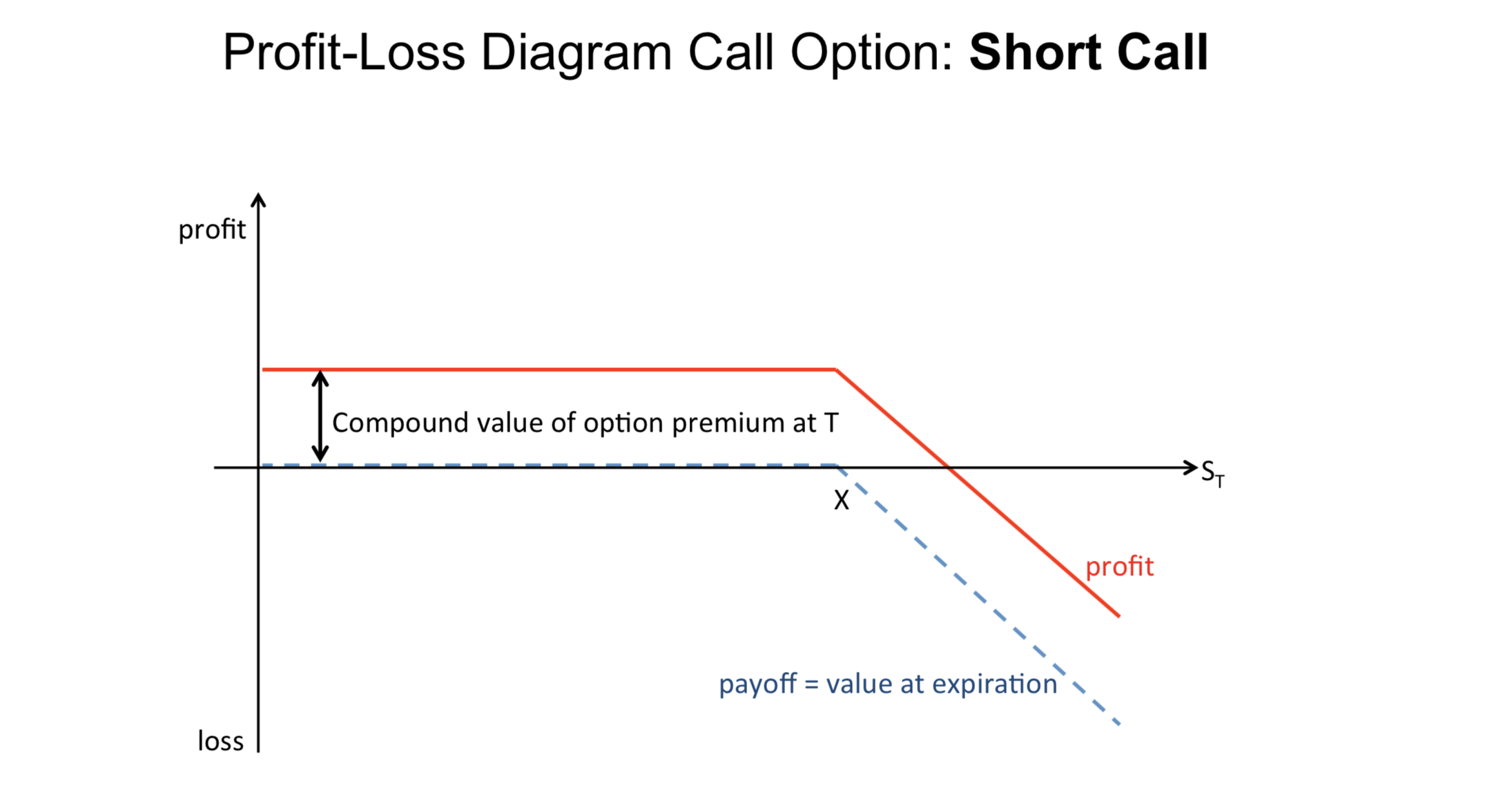

ショート・コール / Short Call

ショート・コールとは、オプション取引においてコール・オプションを売ることをいいます。また、コール・オプションとは、ある商品を将来のある一定期日(期間内)に、その時の市場価格に関係なく、予め決められた一定価格(権利行使価格)で購入することができる権利をいいます。

一般にショート・コールでは、期待通りに原資産の価格が上昇しない場合は、プレミアム(利益)を手に入れることができますが、その一方で原資産の価格が権利行使価格を超えて上昇した場合は、オプションの所有者に権利が行使されないため損失(理論上無制限)となります。

Short call is the option to sell call options. Call options is the right to purchase a specified amount of the underlying at a specified 'exercise price' at or before a specified expiration date.

On short call, generally speaking, if the price of the underlying does not increase as expected, option writers can get premium. On the other hand, if the price of the underlying achieves the exercise price of option, option writers get financial loss (theoretically unlimited) because the right is exercised by holders.

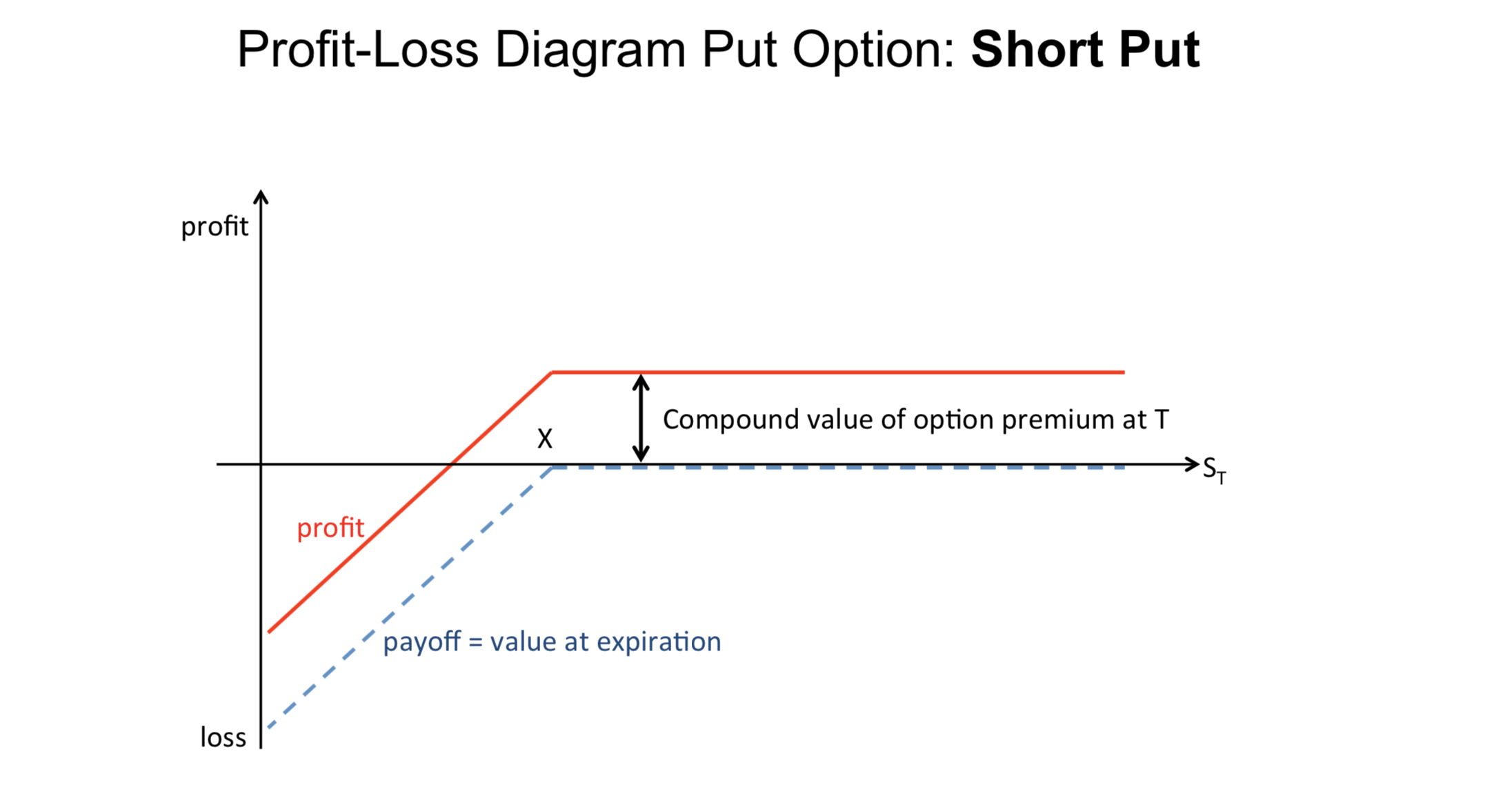

ショート・プット / Short Put

ショート・プットは、オプション取引において、プット・オプションを売ることをいいます。また、プット・オプションとは、ある商品を将来のある一定期日(期間中)に、その時の市場価格に関係なく、予め決められた一定価格(権利行使価格)で売却することができる権利をいいます。

一般にショート・プットでは、期待通りに原資産の価格が下落しない場合は、プレミアム(利益)を手に入れることができますが、その一方で原資産の価格が権利行使価格を超えて下落した場合は、損失となります。

Short put is the option to sell put options. Put options is the right to sell a specified amount of the underlying at a specified 'exercise price' at or before a specified expiration date.

On long put, generally speaking, if the price of the underlying does not decrease as expected, option writers can get premium. On the other hand, if the price of the underlying achieves the expected price, option writers get financial loss (theoretically unlimited) because the right is exercised by holders.

オプション戦略 / Option strategies

強気:

資産運用(投資)において、先行き相場が上昇すると予測する考え方(心理)のこと、または相場が上昇するという見通しが大勢を占めること。(例:ロング・コールやショート・プット)

弱気:資産運用(投資)において、先行き相場が下落すると予測する考え方(心理)のこと、または相場が下落するという見通しが大勢を占めること

Bullish strategy:

The expectation that investors can generate a profit when the underlying's price increases. (e.g. long call, short put)

Bearish strategy:

The expectation that investors can generate a profit when the underlying's price decreases. (e.g. long put, short call)

4. 続き / Next Article

金融経済学#2:Option Valuation