概要

LSTMを使用した株価予測サンプルをかなり前に試してみたのですが

放置状態なっていたので、忘れないうちにメモを残しておきます。

※参考元はPython2系、ipynb形式ですが

今回はPython3系、py形式で動かせるように修正し試しました

・環境情報

Windows10 Pro

Anaconda 1.9.X

Python 3.6.X

keras 2.2.4

numpy 1.15.4

Visual studio Code

実施手順

1.実施環境

下記はインストール済みであることが前提

Anaconda1.9.X

Python 3.6.X

keras 2.2.4

numpy 1.15.4

実行アプリは以下を使用

Visual studio Code

2.学習アプリの準備

以下URLから「Clone or Download」をクリックし「How-to-Predict-Stock-Prices-Easily-Demo-master.zip」をダウンロード

https://github.com/llSourcell/How-to-Predict-Stock-Prices-Easily-Demo

上記ダウンロードファイルを解凍し、フォルダを任意の場所に配置

上記解凍フォルダに以下の2つのソースコード「stockdemo.py」「lstm.py」を置く

※Python2.X系、Jupyter Notebook の場合は「stockdemo.ipynb」で実行できるはず?

from keras.layers.core import Dense, Activation, Dropout

from keras.layers.recurrent import LSTM

from keras.models import Sequential

import lstm, time #helper libraries

#Step 1 Load Data

X_train, y_train, X_test, y_test = lstm.load_data('sp500.csv', 50, True)

#Step 2 Build Model

model = Sequential()

model.add(LSTM(

input_dim=1,

output_dim=50,

return_sequences=True))

model.add(Dropout(0.2))

model.add(LSTM(

100,

return_sequences=False))

model.add(Dropout(0.2))

model.add(Dense(

output_dim=1))

model.add(Activation('linear'))

start = time.time()

model.compile(loss='mse', optimizer='rmsprop')

print('compilation time : ', time.time() - start)

#Step 3 Train the model

model.fit(

X_train,

y_train,

batch_size=512,

nb_epoch=1,

validation_split=0.05)

#Step 4 - Plot the predictions!

predictions = lstm.predict_sequences_multiple(model, X_test, 50, 50)

lstm.plot_results_multiple(predictions, y_test, 50)

import time

import warnings

import numpy as np

from numpy import newaxis

from keras.layers.core import Dense, Activation, Dropout

from keras.layers.recurrent import LSTM

from keras.models import Sequential

import matplotlib.pyplot as plt

warnings.filterwarnings("ignore")

def plot_results_multiple(predicted_data, true_data, prediction_len):

fig = plt.figure(facecolor='white')

ax = fig.add_subplot(111)

ax.plot(true_data, label='True Data')

print('yo')

#Pad the list of predictions to shift it in the graph to it's correct start

for i, data in enumerate(predicted_data):

padding = [None for p in range(i * prediction_len)]

plt.plot(padding + data, label='Prediction')

plt.legend()

plt.show()

def load_data(filename, seq_len, normalise_window):

f = open(filename, 'r').read()

data = f.split('\n')

sequence_length = seq_len + 1

result = []

for index in range(len(data) - sequence_length):

result.append(data[index: index + sequence_length])

if normalise_window:

result = normalise_windows(result)

result = np.array(result)

row = round(0.9 * result.shape[0])

train = result[:int(row), :]

np.random.shuffle(train)

x_train = train[:, :-1]

y_train = train[:, -1]

x_test = result[int(row):, :-1]

y_test = result[int(row):, -1]

x_train = np.reshape(x_train, (x_train.shape[0], x_train.shape[1], 1))

x_test = np.reshape(x_test, (x_test.shape[0], x_test.shape[1], 1))

return [x_train, y_train, x_test, y_test]

def normalise_windows(window_data):

normalised_data = []

for window in window_data:

normalised_window = [((float(p) / float(window[0])) - 1) for p in window]

normalised_data.append(normalised_window)

return normalised_data

def build_model(layers):

model = Sequential()

model.add(LSTM(

input_dim=layers[0],

output_dim=layers[1],

return_sequences=True))

model.add(Dropout(0.2))

model.add(LSTM(

layers[2],

return_sequences=False))

model.add(Dropout(0.2))

model.add(Dense(

output_dim=layers[3]))

model.add(Activation("linear"))

start = time.time()

model.compile(loss="mse", optimizer="rmsprop")

print("Compilation Time : ", time.time() - start)

return model

def predict_point_by_point(model, data):

#Predict each timestep given the last sequence of true data, in effect only predicting 1 step ahead each time

predicted = model.predict(data)

predicted = np.reshape(predicted, (predicted.size,))

return predicted

def predict_sequence_full(model, data, window_size):

#Shift the window by 1 new prediction each time, re-run predictions on new window

curr_frame = data[0]

predicted = []

for i in range(len(data)):

predicted.append(model.predict(curr_frame[newaxis,:,:])[0,0])

curr_frame = curr_frame[1:]

curr_frame = np.insert(curr_frame, [window_size-1], predicted[-1], axis=0)

return predicted

def predict_sequences_multiple(model, data, window_size, prediction_len):

#Predict sequence of 50 steps before shifting prediction run forward by 50 steps

prediction_seqs = []

for i in range((int)(len(data)/prediction_len)):

curr_frame = data[i*prediction_len]

predicted = []

for j in range(prediction_len):

predicted.append(model.predict(curr_frame[newaxis,:,:])[0,0])

curr_frame = curr_frame[1:]

curr_frame = np.insert(curr_frame, [window_size-1], predicted[-1], axis=0)

prediction_seqs.append(predicted)

return prediction_seqs

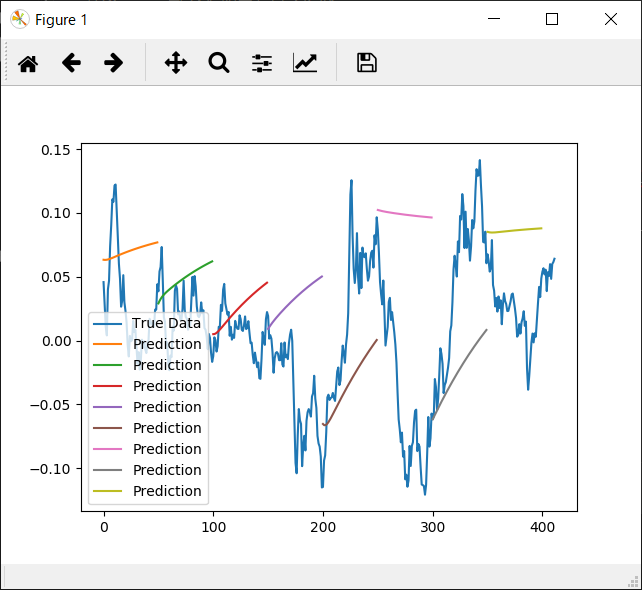

3.実行と結果確認

stockdemo.pyを実行すると、以下のように結果がグラフで表示される

※predictionとなっているところが、LSTMによる予測

以上

参考文献

https://futurismo.biz/archives/6389/

https://github.com/llSourcell/How-to-Predict-Stock-Prices-Easily-Demo

python V2→V3差分修正

http://diveintopython3-ja.rdy.jp/porting-code-to-python-3-with-2to3.html