OLS、特徴選択、リッジ回帰、ラッソの4つの方法でTrainデータからモデルをFittingし、Testデータを用いて、平均2乗誤差(MSE)を推定して比べるといったことをします。

まずはデータの準備

データはStanford大学の統計学部からprostateのデータをダウンロード、正規化、訓練データ、テストデータに分けて使います。

> # Download prostate data

> con = "http://statweb.stanford.edu/~tibs/ElemStatLearn/datasets/prostate.data"

> prostate=read.csv(con,row.names=1,sep="\t")

>

> # Scale data and prepare train/test split

> prost.std <- data.frame(cbind(scale(prostate[,1:8]),prostate$lpsa))

> names(prost.std)[9] <- 'lpsa'

> data.train <- prost.std[prostate$train,]

> data.test <- prost.std[!prostate$train,]

> y.test <- data.test$lpsa

> n.train <- nrow(data.train)

OLS

単純な最小二乗法でMSEを求めてみます。

> m.ols <- lm(lpsa ~ . , data=data.train)

> summary(m.ols)

Call:

lm(formula = lpsa ~ ., data = data.train)

Residuals:

Min 1Q Median 3Q Max

-1.64870 -0.34147 -0.05424 0.44941 1.48675

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 2.46493 0.08931 27.598 < 2e-16 ***

lcavol 0.67953 0.12663 5.366 1.47e-06 ***

lweight 0.26305 0.09563 2.751 0.00792 **

age -0.14146 0.10134 -1.396 0.16806

lbph 0.21015 0.10222 2.056 0.04431 *

svi 0.30520 0.12360 2.469 0.01651 *

lcp -0.28849 0.15453 -1.867 0.06697 .

gleason -0.02131 0.14525 -0.147 0.88389

pgg45 0.26696 0.15361 1.738 0.08755 .

---

Signif. codes:

0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

Residual standard error: 0.7123 on 58 degrees of freedom

Multiple R-squared: 0.6944, Adjusted R-squared: 0.6522

F-statistic: 16.47 on 8 and 58 DF, p-value: 2.042e-12

> y.pred.ols <- predict(m.ols,data.test)

> summary((y.pred.ols - y.test)^2)

Min. 1st Qu. Median Mean 3rd Qu. Max.

0.000209 0.044030 0.116400 0.521300 0.445000 4.097000

>

> mse.ols=sum((y.pred.ols - y.test)^2)

> mse.ols

[1] 15.63822

特徴選択

次に特徴量を減らしてみます。

leap関数でCp(Process Capability Index)をもとに特徴選択を行った上で、MSEを求めます。

whichで確認すると、gleasonを削ったモデルが良さそうだと判断されてます。

> library(leaps)

> l <- leaps(data.train[,1:8],data.train[,9],method='Cp')

> plot(l$size,l$Cp)

>

> # Select best model according to Cp

> bestfeat <- l$which[which.min(l$Cp),]

> bestfeat

1 2 3 4 5 6 7 8

TRUE TRUE TRUE TRUE TRUE TRUE FALSE TRUE

>

> # Train and test the model on the best subset

> m.bestsubset <- lm(lpsa ~ .,data=data.train[,bestfeat])

> summary(m.bestsubset)

Call:

lm(formula = lpsa ~ ., data = data.train[, bestfeat])

Residuals:

Min 1Q Median 3Q Max

-1.65425 -0.34471 -0.05615 0.44380 1.48952

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 2.46687 0.08760 28.161 < 2e-16 ***

lcavol 0.67645 0.12384 5.462 9.88e-07 ***

lweight 0.26528 0.09363 2.833 0.0063 **

age -0.14503 0.09757 -1.486 0.1425

lbph 0.20953 0.10128 2.069 0.0430 *

svi 0.30709 0.12190 2.519 0.0145 *

lcp -0.28722 0.15300 -1.877 0.0654 .

pgg45 0.25228 0.11562 2.182 0.0331 *

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

Residual standard error: 0.7064 on 59 degrees of freedom

Multiple R-squared: 0.6943, Adjusted R-squared: 0.658

F-statistic: 19.14 on 7 and 59 DF, p-value: 4.496e-13

> y.pred.bestsubset <- predict(m.bestsubset,data.test[,bestfeat])

> summary((y.pred.bestsubset - y.test)^2)

Min. 1st Qu. Median Mean 3rd Qu. Max.

0.000575 0.038000 0.122400 0.516500 0.449300 4.002000

>

> mse.bestsubset=sum((y.pred.bestsubset - y.test)^2)

> mse.bestsubset

[1] 15.4954

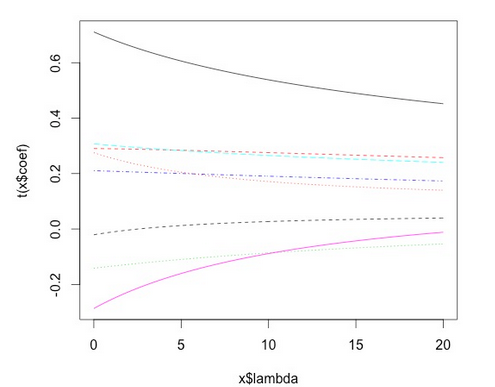

リッジ回帰

次にリッジ回帰でやってみます。

リッジ回帰とラッソについて、なんだっけという場合は下記がご参考。

で、さくっとやってみます。

> library(MASS)

> m.ridge <- lm.ridge(lpsa ~ .,data=data.train, lambda = seq(0,20,0.1))

> plot(m.ridge)

>

> #by using the select function

> select(m.ridge)

modified HKB estimator is 3.355691

modified L-W estimator is 3.050708

smallest value of GCV at 4.9

下記のような図と共に、ベストなλは4.9だと選ばれました。

次に予測値を返させて、MSEを求めます。

> y.pred.ridge = scale(data.test[,1:8],center = m.ridge$xm, scale = m.ridge$scales)%*% m.ridge$coef[,which.min(m.ridge$GCV)] + m.ridge$ym

> summary((y.pred.ridge - y.test)^2)

V1

Min. :0.000003

1st Qu.:0.043863

Median :0.136450

Mean :0.494410

3rd Qu.:0.443495

Max. :3.809051

> mse.ridge=sum((y.pred.ridge - y.test)^2)

> mse.ridge

[1] 14.8323

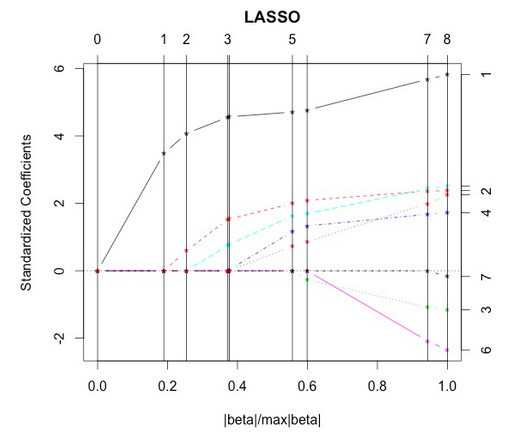

ラッソ

あまり使っている見ませんが、larsライブラリー([https://cran.r-project.org/web/packages/lars/index.html])を使います。

> library(lars)

> m.lasso <- lars(as.matrix(data.train[,1:8]),data.train$lpsa,type="lasso")

> plot(m.lasso)

> # Cross-validation

> r <- cv.lars(as.matrix(data.train[,1:8]),data.train$lpsa)

> bestfraction <- r$index[which.min(r$cv)]

> bestfraction

[1] 0.5252525

fractionは0.525あたりと図と出力から判断出来ます。

> # Observe coefficients

> coef.lasso <- predict(m.lasso,as.matrix(data.test[,1:8]),s=bestfraction,type="coefficient",mode="fraction")

>

> # Prediction

> y.pred.lasso <- predict(m.lasso,as.matrix(data.test[,1:8]),s=bestfraction,type="fit",mode="fraction")$fit

> summary((y.pred.lasso - y.test)^2)

Min. 1st Qu. Median Mean 3rd Qu. Max.

0.000144 0.072470 0.128000 0.454000 0.394400 3.565000

>

> mse.lasso=sum((y.pred.lasso - y.test)^2)

> mse.lasso

[1] 13.61874

平均二乗誤差の比較

> # Compare them

> mse.ols

[1] 15.63822

> mse.bestsubset

[1] 15.4954

> mse.ridge

[1] 14.8323

> mse.lasso

[1] 13.61874

今回のデータに関しては、ラッソで行った分析が一番MSEを最小に出来ました。