※ 自分用

つらつらと自分用のPython Tipsが並ぶだけで説明はありません。

随時更新で徐々に充実させていく用途です。

from __future__ import division, unicode_literals

一般

# リストの要素毎に数を数える

from collections import defaultdict

cnt_dict = defaultdict(int)

data = x = np.random.randint(low=0, high=5, size=500)

for d in data:

cnt_dict[d] += 1

print cnt_dict

out

defaultdict(<type 'int'>, {0: 90, 1: 113, 2: 94, 3: 96, 4: 107})

- 利用ライブラリのバージョンチェックと不適合の場合のアサート

# ライブラリのバージョンチェック

from distutils.version import LooseVersion

# 使用例

assert LooseVersion(tf.__version__) >= LooseVersion("1.3")

# もっと便利なカウントの仕方

import numpy as np

from collections import Counter

data1 = np.random.randint(low=0, high=5, size=300)

cnt1 = Counter(data1)

print cnt1

data2 = np.random.randint(low=0, high=10, size=500)

cnt2 = Counter(data2)

print cnt2

print cnt1 + cnt2

out

Counter({3: 65, 0: 64, 1: 60, 4: 60, 2: 51})

Counter({4: 58, 8: 58, 1: 55, 6: 54, 0: 53, 2: 49, 3: 47, 5: 46, 7: 40, 9: 40})

Counter({4: 118, 0: 117, 1: 115, 3: 112, 2: 100, 8: 58, 6: 54, 5: 46, 7: 40, 9: 40})

# Pickleする

import cPickle as pickle

def unpickle(filename):

with open(filename, 'rb') as fo:

_dict = pickle.load(fo)

return _dict

def to_pickle(filename, obj):

with open(filename, 'wb') as f:

pickle.dump(obj, f, -1)

# pickle.Pickler(f, 2).dump(obj)

# webページからリンクの抽出

from bs4 import BeautifulSoup

import requests

from requests_oauthlib import OAuth1Session

url = 'http://headlines.yahoo.co.jp/rss/list'

url_list = []

res = requests.get(url)

news_all = BeautifulSoup(res.text, "xml")

for link in news_all.find_all('a'):

url = link.get('href')

print url

h5でsave&load

import deepdish as dd

dd.io.save("../data/df_test.h5", df_test)

df_test = dd.io.load("../data/df_test.h5")

# 小数点第何位まで表示するか

%precision 4

np.pi

out

3.1416

描画関連

# 定型インポート文

%matplotlib inline

import matplotlib.pyplot as plt

import numpy as np

import pandas as pd

from datetime import diatomite as dt

import sys

plt.style.use('ggplot')

# Texを使う時

plt.rc('text', usetex=True)

plt.rc('font', family='serif')

Pandas Dataframe

数字に見える文字列を、数値型に変換する

# http://stackoverflow.com/questions/21197774/assign-pandas-dataframe-column-dtypes

In [11]: df

Out[11]:

x y

0 a 1

1 b 2

In [12]: df.dtypes

Out[12]:

x object

y object

dtype: object

In [13]: df.convert_objects(convert_numeric=True)

Out[13]:

x y

0 a 1

1 b 2

In [14]: df.convert_objects(convert_numeric=True).dtypes

Out[14]:

x object

y int64

dtype: object

# カテゴリ変数(Rで言うfactory型)的な扱いについて

%matplotlib inline

from matplotlib import pyplot as plt

import numpy as np

import pandas as pd

import seaborn as sns

sns.set()

df = sns.load_dataset("tips")

for c in ['sex', 'smoker', 'day', 'time',]:

df["c{}".format(c)] = pd.Categorical.from_array(df[c]).codes

df.head()

out

total_bill tip sex smoker day time size csex csmoker cday ctime

0 16.99 1.01 Female No Sun Dinner 2 0 0 2 0

1 10.34 1.66 Male No Sun Dinner 3 1 0 2 0

2 21.01 3.50 Male No Sun Dinner 3 1 0 2 0

3 23.68 3.31 Male No Sun Dinner 2 1 0 2 0

4 24.59 3.61 Female No Sun Dinner 4 0 0 2 0

日付関連

from datetime import datetime

now = datetime.now()

now.strftime("%Y-%m-%d %a %H:%M:%S")

out

'2015-08-13 Thu 16:41:25'

from dateutil.parser import parse

parse("2015-3-25 21:43:15")

out

datetime.datetime(2015, 3, 25, 21, 43, 15)

datestrs = ['2011/7/6 12:00:00', None, '2011/8/6 21:00:00']

pd.to_datetime(datestrs)

out

DatetimeIndex(['2011-07-06 12:00:00', 'NaT', '2011-08-06 21:00:00'], dtype='datetime64[ns]', freq=None, tz=None)

# 日付重複チェック

dates = pd.DatetimeIndex(['2000/1/1', '2000/1/2', '2000/1/2', '2000/1/2','2000/1/3'])

dup_ts = pd.Series(np.arange(5), index=dates)

dup_ts.index.is_unique

out

False

dup_ts.groupby(level=0).count()

out

2000-01-01 1

2000-01-02 3

2000-01-03 1

# 範囲指定で日付データ生成

dft = pd.date_range(start='2000-1-1', end='2001-1-1', freq='H')

dft

out

DatetimeIndex(['2000-01-01 00:00:00', '2000-01-01 01:00:00',

'2000-01-01 02:00:00', '2000-01-01 03:00:00',

'2000-01-01 04:00:00', '2000-01-01 05:00:00',

'2000-01-01 06:00:00', '2000-01-01 07:00:00',

'2000-01-01 08:00:00', '2000-01-01 09:00:00',

...

'2000-12-31 15:00:00', '2000-12-31 16:00:00',

'2000-12-31 17:00:00', '2000-12-31 18:00:00',

'2000-12-31 19:00:00', '2000-12-31 20:00:00',

'2000-12-31 21:00:00', '2000-12-31 22:00:00',

'2000-12-31 23:00:00', '2001-01-01 00:00:00'],

dtype='datetime64[ns]', length=8785, freq='H', tz=None)

# 日付の抜けを埋める(resample関数)

dates = pd.DatetimeIndex(['2000/1/1', '2000/1/5', '2000/1/8', '2000/1/9'])

df = pd.DataFrame(np.random.normal(0,1,size=len(dates)), columns=["num"], index=dates)

print "[Before]"

print df

df = df.resample('D')

print "[After]"

print df

out

[Before]

num

2000-01-01 1.201939

2000-01-05 0.522156

2000-01-08 1.800669

2000-01-09 -0.834700

[After]

num

2000-01-01 1.201939

2000-01-02 NaN

2000-01-03 NaN

2000-01-04 NaN

2000-01-05 0.522156

2000-01-06 NaN

2000-01-07 NaN

2000-01-08 1.800669

2000-01-09 -0.834700

# ローカライゼーション

dates = pd.DatetimeIndex(['2000/1/1', '2000/1/5', '2000/1/8', '2000/1/9'])

print dates.tz.__repr__

print dates

# 日本時間にロケーションを設定(ex:00:00:00が日本時間での時刻と認識される)

dates = dates.tz_localize("Japan")

print dates

# US東海岸時間に変換(値は変わらない)

print dates.tz_convert('US/Eastern')

out

<method-wrapper '__repr__' of NoneType object at 0x10017dc40>

DatetimeIndex(['2000-01-01', '2000-01-05', '2000-01-08', '2000-01-09'], dtype='datetime64[ns]', freq=None, tz=None)

DatetimeIndex(['2000-01-01 00:00:00+09:00', '2000-01-05 00:00:00+09:00',

'2000-01-08 00:00:00+09:00', '2000-01-09 00:00:00+09:00'],

dtype='datetime64[ns]', freq=None, tz='Japan')

DatetimeIndex(['1999-12-31 10:00:00-05:00', '2000-01-04 10:00:00-05:00',

'2000-01-07 10:00:00-05:00', '2000-01-08 10:00:00-05:00'],

dtype='datetime64[ns]', freq=None, tz='US/Eastern')

rng = pd.period_range('2014/1/1', '2015/3/31', freq='M');

print rng

ser = pd.Series(np.random.randn(rng.size), index=rng)

print ser

values = ['2014Q3','2014Q4','2015Q1', '2015Q2']

index = pd.PeriodIndex(values, freq='Q-DEC')

df = pd.DataFrame(np.random.randn(index.size), index=index)

print df

out

PeriodIndex(['2014-01', '2014-02', '2014-03', '2014-04', '2014-05', '2014-06',

'2014-07', '2014-08', '2014-09', '2014-10', '2014-11', '2014-12',

'2015-01', '2015-02', '2015-03'],

dtype='int64', freq='M')

2014-01 0.273280

2014-02 -0.231141

2014-03 0.251094

2014-04 -1.217927

2014-05 0.341373

2014-06 -0.931357

2014-07 -0.414243

2014-08 -1.876341

2014-09 1.152908

2014-10 -0.473921

2014-11 0.527473

2014-12 -0.529911

2015-01 -0.656616

2015-02 0.742319

2015-03 -0.268112

Freq: M, dtype: float64

0

2014Q3 0.011621

2014Q4 -0.029027

2015Q1 -0.222156

2015Q2 -0.749983

# CYを適用した場合

values = ['2014Q3','2014Q4','2015Q1', '2015Q2']

index = pd.PeriodIndex(values, freq='Q-DEC')

print index

print index.asfreq('M',how='start')

print index.asfreq('M',how='end')

print index.asfreq('D',how='start')

print index.asfreq('D',how='end')

out

PeriodIndex(['2014Q3', '2014Q4', '2015Q1', '2015Q2'], dtype='int64', freq='Q-DEC')

PeriodIndex(['2014-07', '2014-10', '2015-01', '2015-04'], dtype='int64', freq='M')

PeriodIndex(['2014-09', '2014-12', '2015-03', '2015-06'], dtype='int64', freq='M')

PeriodIndex(['2014-07-01', '2014-10-01', '2015-01-01', '2015-04-01'], dtype='int64', freq='D')

PeriodIndex(['2014-09-30', '2014-12-31', '2015-03-31', '2015-06-30'], dtype='int64', freq='D')

# FYを適用した場合

values = ['2014Q3','2014Q4','2015Q1', '2015Q2']

index = pd.PeriodIndex(values, freq='Q-MAR')

print index

print index.asfreq('M',how='start')

print index.asfreq('M',how='end')

print index.asfreq('D',how='start')

print index.asfreq('D',how='end')

out

PeriodIndex(['2014Q3', '2014Q4', '2015Q1', '2015Q2'], dtype='int64', freq='Q-MAR')

PeriodIndex(['2013-10', '2014-01', '2014-04', '2014-07'], dtype='int64', freq='M')

PeriodIndex(['2013-12', '2014-03', '2014-06', '2014-09'], dtype='int64', freq='M')

PeriodIndex(['2013-10-01', '2014-01-01', '2014-04-01', '2014-07-01'], dtype='int64', freq='D')

PeriodIndex(['2013-12-31', '2014-03-31', '2014-06-30', '2014-09-30'], dtype='int64', freq='D')

# time zone change from utc to stdjp (for no timezone variable)

import datetime, pytz

utc = pytz.timezone('UTC')

jst = pytz.timezone('Asia/Tokyo')

now = datetime.datetime.now()

updated = now.replace(tzinfo=utc).astimezone(jst)

print "time:{}".format(updated)

out

time:2015-08-22 02:46:23.844806+09:00

out

out

時系列

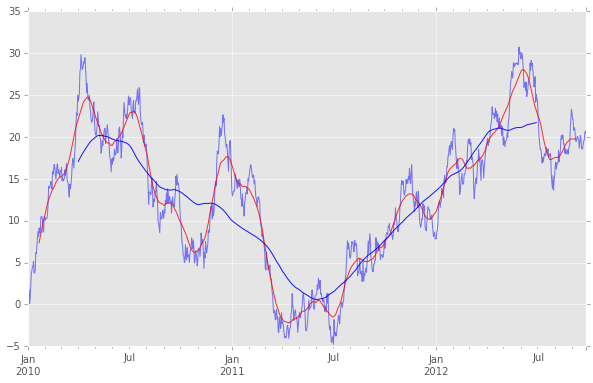

ts = pd.Series(np.random.randn(1000), index=pd.date_range('2010/1/1', periods=1000))

ts = ts.cumsum()

ts.plot(color="b", alpha=0.5, figsize=(10,6))

# 単純移動平均

pd.rolling_mean(ts, 40, center=True).plot(style='-', c='r', alpha=0.8,)

pd.rolling_mean(ts, 180, center=True).plot(style='-', c='blue', alpha=0.9,zorder=100)

# 日付でスライスできる!

ts['2010/12/31':]

out

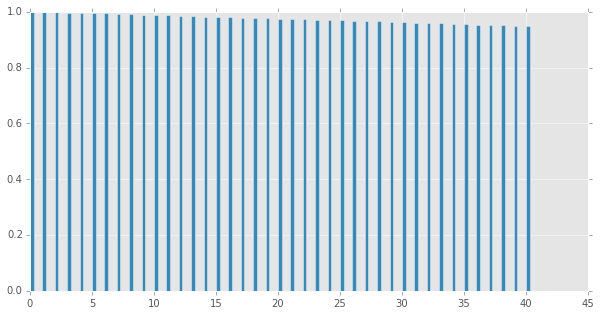

# コレログラムの描画

import statsmodels.tsa.stattools as stt

plt.figure(figsize=(10,5))

acf = stt.acf(np.array(ts), 60) #ACF算出

plt.bar(range(len(acf)), acf, width = 0.3) #表示

plt.show()

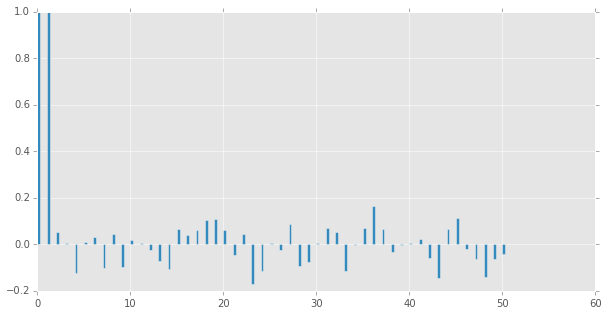

pcf = stt.pacf(np.array(ts), 50)

plt.figure(figsize=(10,5))

plt.bar(range(len(pcf)), pcf, width = 0.3)

plt.show()

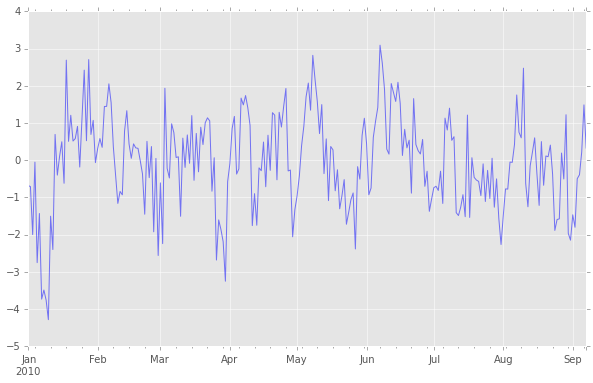

# ARMA(3, 0)過程のサンプル生成

from statsmodels.tsa.arima_process import arma_generate_sample

ar_params = np.array([0.30, 0.50, -0.10])

ma_params = np.array([0.00])

ar_params = np.r_[1, -ar_params]

ma_params = np.r_[1, -ma_params]

nobs = 250

y = arma_generate_sample(ar_params, ma_params, nobs)

ts = pd.Series(y, index=pd.date_range('2010/1/1', periods=nobs))

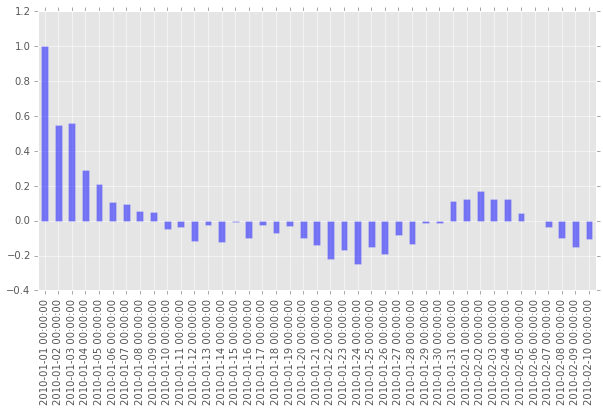

ts.plot(color="b", alpha=0.5, figsize=(10,6))

plt.figure(figsize=(10,5))

acf = stt.acf(np.array(ts), 60) #ACF算出

ts_acf = pd.Series(acf, index=pd.date_range('2010/1/1', periods=len(acf)))

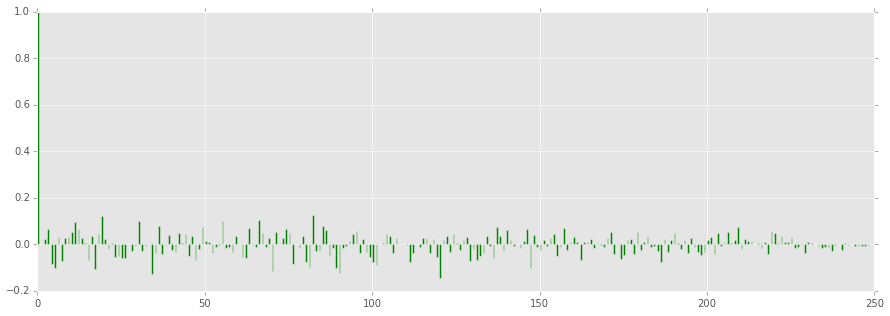

ts_acf.plot(kind='bar', figsize=(10,5), color="b", alpha=0.5)

plt.show()

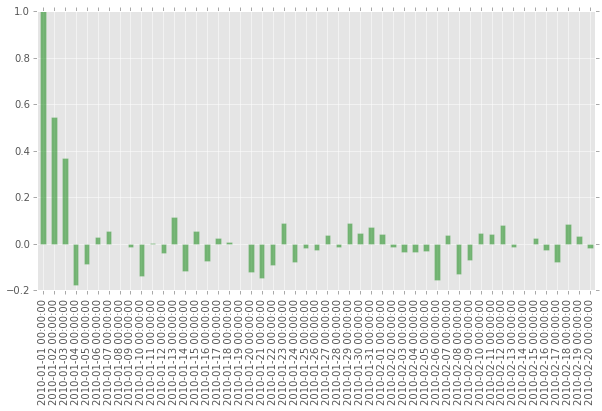

pacf = stt.pacf(np.array(ts), 50)

ts_pacf = pd.Series(pacf, index=pd.date_range('2010/1/1', periods=len(pacf)))

ts_pacf.plot(kind='bar', figsize=(10,5), color="g", alpha=0.5)

plt.show()

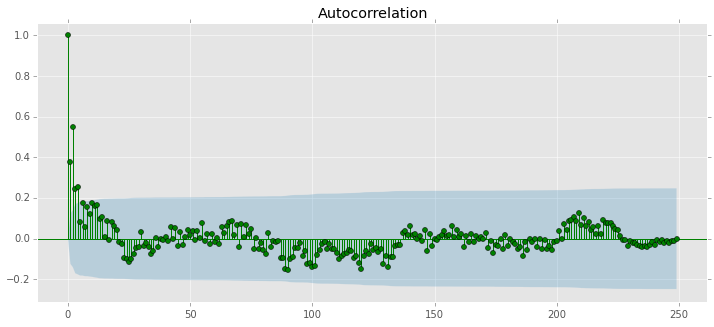

import statsmodels.graphics.tsaplots as tsaplots

fig = plt.figure(figsize=(12,5))

ax = fig.add_subplot(111)

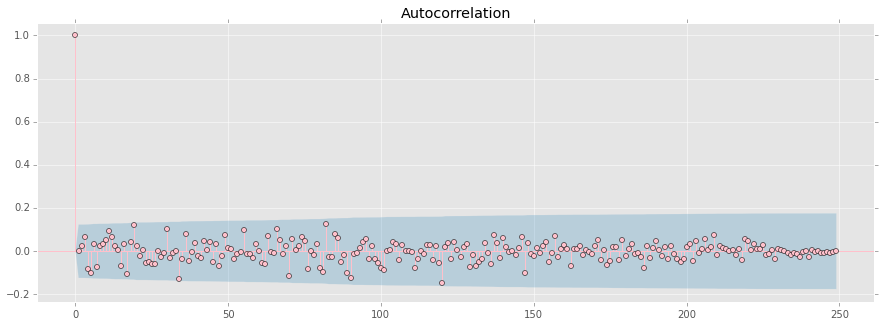

tsaplots.plot_acf(ts, ax=ax, color="g")

plt.show()

# ARMA 検定

from statsmodels.tsa import arima_model

arma = arima_model.ARMA(y, order = [3,0]).fit()

print arma.summary()

out

ARMA Model Results

==============================================================================

Dep. Variable: y No. Observations: 250

Model: ARMA(3, 0) Log Likelihood -357.274

Method: css-mle S.D. of innovations 1.009

Date: Thu, 13 Aug 2015 AIC 724.548

Time: 17:57:45 BIC 742.155

Sample: 0 HQIC 731.634

==============================================================================

coef std err z P>|z| [95.0% Conf. Int.]

------------------------------------------------------------------------------

const 0.0262 0.187 0.140 0.889 -0.341 0.393

ar.L1.y 0.2256 0.063 3.586 0.000 0.102 0.349

ar.L2.y 0.4945 0.057 8.699 0.000 0.383 0.606

ar.L3.y -0.0569 0.064 -0.895 0.371 -0.181 0.068

Roots

=============================================================================

Real Imaginary Modulus Frequency

-----------------------------------------------------------------------------

AR.1 1.2968 +0.0000j 1.2968 0.0000

AR.2 -1.5205 +0.0000j 1.5205 0.5000

AR.3 8.9145 +0.0000j 8.9145 0.0000

-----------------------------------------------------------------------------

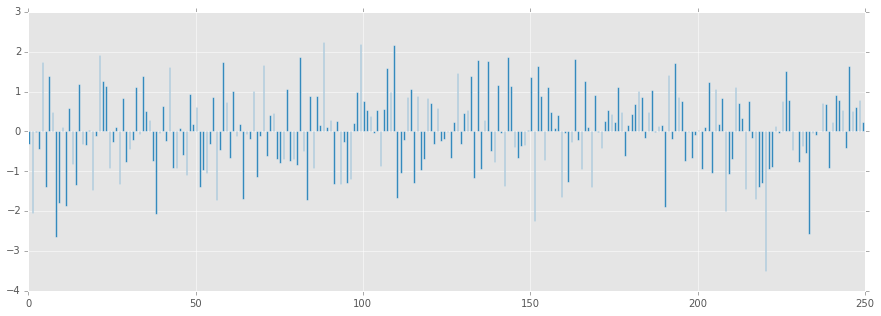

# ARMA残差の確認

resid = arma.resid

plt.figure(figsize=(15,5))

plt.bar(range(len(resid)), resid, width=0.5)

plt.show()

plt.figure(figsize=(15,5))

acf = stt.acf(resid, nlags=len(resid))

plt.bar(range(len(acf)), acf, width=0.5, color="g")

plt.show()

fig = plt.figure(figsize=(15,5))

ax = fig.add_subplot(111)

tsaplots.plot_acf(resid, ax=ax, color="pink")

plt.show()

# Ljung-Box Q-statistic for autocorrelation parameters

lbs = stt.q_stat(acf, len(ts)) #statsmodelsはacfを入力とする仕様

plt.figure(figsize=(12,6))

plt.bar(range(len(lbs[1])), lbs[1])

# 欠損値を0で埋める

df_data.fillna(0)

out

out

Spark

import os, sys

from datetime import datetime as dt

print "loading PySpark setting..."

spark_home = os.environ.get('SPARK_HOME', None)

if not spark_home:

raise ValueError('SPARK_HOME environment variable is not set')

sys.path.insert(0, os.path.join(spark_home, 'python'))

sys.path.insert(0, os.path.join(spark_home, 'python/lib/py4j-0.8.2.1-src.zip'))

execfile(os.path.join(spark_home, 'python/pyspark/shell.py'))

out

loading PySpark setting...

Welcome to

____ __

/ __/__ ___ _____/ /__

_\ \/ _ \/ _ `/ __/ '_/

/__ / .__/\_,_/_/ /_/\_\ version 1.5.0

/_/

Using Python version 2.7.10 (default, May 28 2015 17:04:42)

SparkContext available as sc, HiveContext available as sqlContext.

# Cross Validation用にデータを分割

from pyspark.mllib.regression import LabeledPoint

def parsePoint(vec):

return LabeledPoint(vec[0], vec[1:])

dat = np.column_stack([iris.target[:], iris.data[:,0],iris.data[:,2]])

data = sc.parallelize(dat) # RDD化

parsedData = data.map(parsePoint) # 中身のデータをLabeledPointに変換

# 訓練データとテストデータに分割

(trainingData, testData) = parsedData.randomSplit([0.7, 0.3])

out

out

out

out

out

out

out

out

out

out

out

out

out

out

out

out

out

out

out

out

out

out

out

out

out