『経済・ファイナンスデータの計量時系列分析』

の章末問題で「コンピュータを用いて」とあるものをRで解いています。

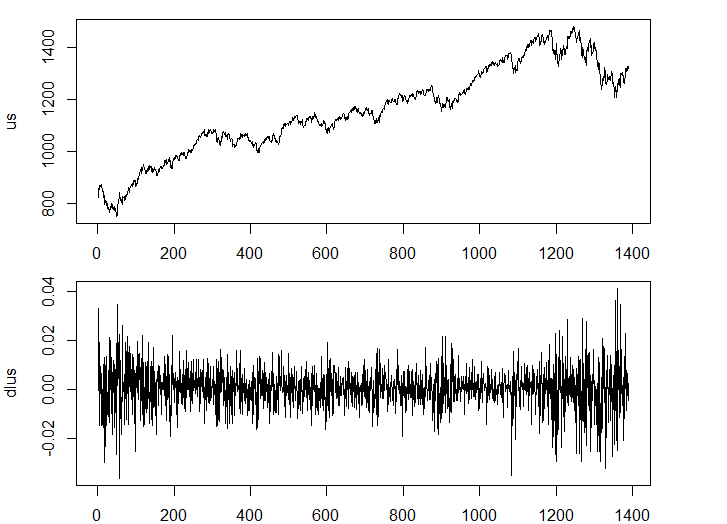

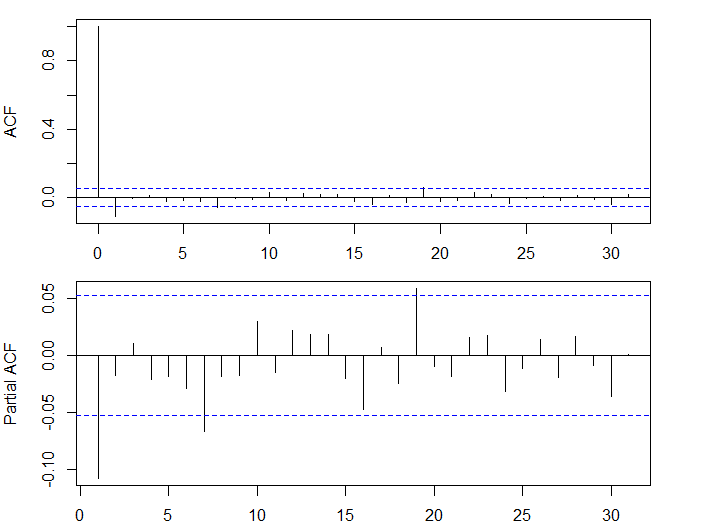

7.4

(1)

- 大きな自己相関はみられない

msci_day<-read.table("msci_day.txt",header=T)

par(mfrow=c(2,1))

us<-msci_day$us

plot(us, type="l")

dlus<-diff(log(us))

plot(dlus, type="l")

acf(dlus)

pacf(dlus)

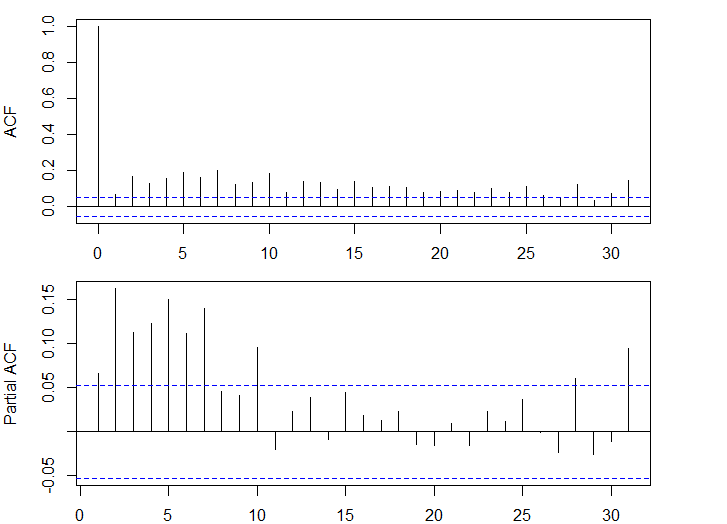

(2)

- 大きな自己相関がみられる

acf(dlus^2)

pacf(dlus^2)

(3)

# fGarch

library(fGarch)

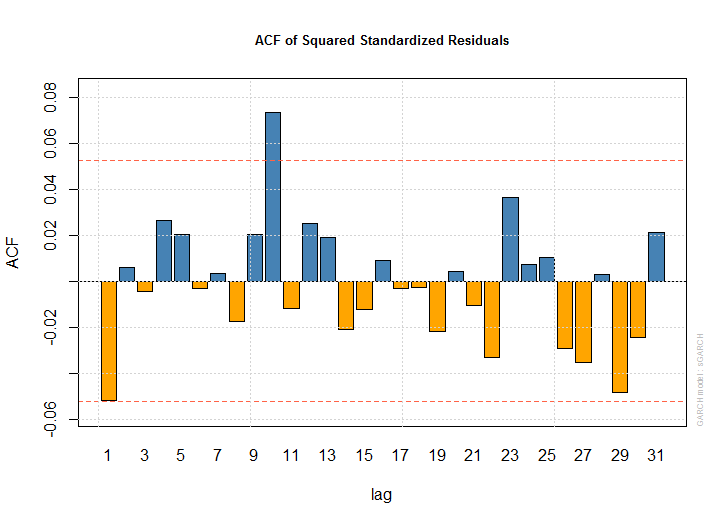

dlus.garch<-garchFit(formula=~arma(1,0)+garch(1,1), data=dlus, trace=F)

summary(dlus.garch)

Title:

GARCH Modelling

Call:

garchFit(formula = ~arma(1, 0) + garch(1, 1), data = dlus, trace = F)

Mean and Variance Equation:

data ~ arma(1, 0) + garch(1, 1)

<environment: 0x0000000015605008>

[data = dlus]

Conditional Distribution:

norm

Coefficient(s):

mu ar1 omega alpha1

4.6782e-04 -7.8543e-02 1.0128e-06 5.0598e-02

beta1

9.3444e-01

Std. Errors:

based on Hessian

Error Analysis:

Estimate Std. Error t value Pr(>|t|)

mu 4.678e-04 1.961e-04 2.386 0.01704 *

ar1 -7.854e-02 2.795e-02 -2.810 0.00495 **

omega 1.013e-06 3.489e-07 2.903 0.00370 **

alpha1 5.060e-02 9.937e-03 5.092 3.55e-07 ***

beta1 9.344e-01 1.314e-02 71.103 < 2e-16 ***

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

Log Likelihood:

4756.516 normalized: 3.421954

Description:

Sun Jan 29 10:00:51 2017 by user: aoki

Standardised Residuals Tests:

Statistic p-Value

Jarque-Bera Test R Chi^2 180.9516 0

Shapiro-Wilk Test R W 0.9840602 2.999756e-11

Ljung-Box Test R Q(10) 10.05805 0.4354152

Ljung-Box Test R Q(15) 14.6652 0.4757913

Ljung-Box Test R Q(20) 17.64631 0.6106947

Ljung-Box Test R^2 Q(10) 13.96237 0.174715

Ljung-Box Test R^2 Q(15) 16.33594 0.3600828

Ljung-Box Test R^2 Q(20) 17.08671 0.6473361

LM Arch Test R TR^2 15.48142 0.2161583

Information Criterion Statistics:

AIC BIC SIC HQIC

-6.836714 -6.817875 -6.836740 -6.829669

# rugarch

library(rugarch)

dlus.spec<-ugarchspec(variance.model=list(model="sGARCH", garchOrder=c(1,1)), mean.model=list(armaOrder=c(1,0), include.mean=T))

dlus.garch<-ugarchfit(data=dlus, spec=dlus.spec)

dlus.garch

> dlus.garch

*---------------------------------*

* GARCH Model Fit *

*---------------------------------*

Conditional Variance Dynamics

-----------------------------------

GARCH Model : sGARCH(1,1)

Mean Model : ARFIMA(1,0,0)

Distribution : norm

Optimal Parameters

------------------------------------

Estimate Std. Error t value Pr(>|t|)

mu 0.000441 0.000183 2.41849 0.015585

ar1 -0.079111 0.028059 -2.81940 0.004811

omega 0.000001 0.000002 0.59728 0.550317

alpha1 0.049525 0.020256 2.44490 0.014489

beta1 0.935539 0.023125 40.45591 0.000000

Robust Standard Errors:

Estimate Std. Error t value Pr(>|t|)

mu 0.000441 0.000355 1.243796 0.213575

ar1 -0.079111 0.027009 -2.929059 0.003400

omega 0.000001 0.000030 0.032807 0.973829

alpha1 0.049525 0.330906 0.149664 0.881029

beta1 0.935539 0.390027 2.398653 0.016455

LogLikelihood : 4751.628

*---------------------------------*

* GARCH Model Fit *

*---------------------------------*

Conditional Variance Dynamics

-----------------------------------

GARCH Model : sGARCH(1,1)

Mean Model : ARFIMA(1,0,0)

Distribution : norm

Optimal Parameters

------------------------------------

Estimate Std. Error t value Pr(>|t|)

mu 0.000441 0.000183 2.41849 0.015585

ar1 -0.079111 0.028059 -2.81940 0.004811

omega 0.000001 0.000002 0.59728 0.550317

alpha1 0.049525 0.020256 2.44490 0.014489

beta1 0.935539 0.023125 40.45591 0.000000

Robust Standard Errors:

Estimate Std. Error t value Pr(>|t|)

mu 0.000441 0.000355 1.243796 0.213575

ar1 -0.079111 0.027009 -2.929059 0.003400

omega 0.000001 0.000030 0.032807 0.973829

alpha1 0.049525 0.330906 0.149664 0.881029

beta1 0.935539 0.390027 2.398653 0.016455

LogLikelihood : 4751.628

Information Criteria

------------------------------------

Akaike -6.8297

Bayes -6.8108

Shibata -6.8297

Hannan-Quinn -6.8226

Weighted Ljung-Box Test on Standardized Residuals

------------------------------------

statistic p-value

Lag[1] 0.001242 0.9719

Lag[2*(p+q)+(p+q)-1][2] 0.385088 0.9856

Lag[4*(p+q)+(p+q)-1][5] 1.217200 0.9092

d.o.f=1

H0 : No serial correlation

Weighted Ljung-Box Test on Standardized Squared Residuals

------------------------------------

statistic p-value

Lag[1] 3.730 0.05345

Lag[2*(p+q)+(p+q)-1][5] 4.288 0.22027

Lag[4*(p+q)+(p+q)-1][9] 4.932 0.43945

d.o.f=2

Weighted ARCH LM Tests

------------------------------------

Information Criteria

------------------------------------

Akaike -6.8297

Bayes -6.8108

Shibata -6.8297

Hannan-Quinn -6.8226

Weighted Ljung-Box Test on Standardized Residuals

------------------------------------

statistic p-value

Lag[1] 0.001242 0.9719

Lag[2*(p+q)+(p+q)-1][2] 0.385088 0.9856

Lag[4*(p+q)+(p+q)-1][5] 1.217200 0.9092

d.o.f=1

H0 : No serial correlation

Weighted Ljung-Box Test on Standardized Squared Residuals

------------------------------------

statistic p-value

Lag[1] 3.730 0.05345

Lag[2*(p+q)+(p+q)-1][5] 4.288 0.22027

Lag[4*(p+q)+(p+q)-1][9] 4.932 0.43945

d.o.f=2

Weighted ARCH LM Tests

------------------------------------

Statistic Shape Scale P-Value

ARCH Lag[3] 0.02518 0.500 2.000 0.8739

ARCH Lag[5] 1.14491 1.440 1.667 0.6905

ARCH Lag[7] 1.28023 2.315 1.543 0.8642

Statistic Shape Scale P-Value

ARCH Lag[3] 0.02518 0.500 2.000 0.8739

ARCH Lag[5] 1.14491 1.440 1.667 0.6905

ARCH Lag[7] 1.28023 2.315 1.543 0.8642

Nyblom stability test

------------------------------------

Joint Statistic: 162.9923

Individual Statistics:

mu 0.04725

ar1 0.15181

omega 16.76474

alpha1 0.32187

beta1 0.21276

Asymptotic Critical Values (10% 5% 1%)

Joint Statistic: 1.28 1.47 1.88

Individual Statistic: 0.35 0.47 0.75

Sign Bias Test

------------------------------------

Nyblom stability test

------------------------------------

Joint Statistic: 162.9923

Individual Statistics:

mu 0.04725

ar1 0.15181

omega 16.76474

alpha1 0.32187

beta1 0.21276

Asymptotic Critical Values (10% 5% 1%)

Joint Statistic: 1.28 1.47 1.88

Individual Statistic: 0.35 0.47 0.75

Sign Bias Test

------------------------------------

t-value prob sig

Sign Bias 1.097 0.27267

Negative Sign Bias 1.033 0.30178

Positive Sign Bias 1.795 0.07293 *

Joint Effect 8.666 0.03408 **

Adjusted Pearson Goodness-of-Fit Test:

------------------------------------

group statistic p-value(g-1)

1 20 88.73 5.556e-11

2 30 113.06 7.184e-12

3 40 110.26 1.005e-08

4 50 140.36 9.542e-11

Elapsed time : 1.15019

t-value prob sig

Sign Bias 1.097 0.27267

Negative Sign Bias 1.033 0.30178

Positive Sign Bias 1.795 0.07293 *

Joint Effect 8.666 0.03408 **

Adjusted Pearson Goodness-of-Fit Test:

------------------------------------

group statistic p-value(g-1)

1 20 88.73 5.556e-11

2 30 113.06 7.184e-12

3 40 110.26 1.005e-08

4 50 140.36 9.542e-11

Elapsed time : 1.15019

-

fGarch

mu = 4.678e-04

ar1 =-7.854e-02

omega = 1.013e-06

alpha1= 5.060e-02

beta1 = 9.344e-01 -

rugarch

mu = 0.000441

ar1 =-0.079111

omega = 0.000001

alpha1= 0.049525

beta1 = 0.935539

(4)

dlus.spec<-ugarchspec(variance.model=list(model="gjrGARCH", garchOrder=c(1,1)), mean.model=list(armaOrder=c(1,0), include.mean=T))

dlus.gjr<-ugarchfit(data=dlus, spec=dlus.spec)

dlus.gjr

> dlus.gjr<-ugarchfit(data=dlus, spec=dlus.spec)

> dlus.gjr

*---------------------------------*

* GARCH Model Fit *

*---------------------------------*

Conditional Variance Dynamics

-----------------------------------

GARCH Model : gjrGARCH(1,1)

Mean Model : ARFIMA(1,0,0)

Distribution : norm

Optimal Parameters

------------------------------------

Estimate Std. Error t value Pr(>|t|)

mu 0.000245 0.000183 1.340180 0.180187

ar1 -0.074942 0.027716 -2.703945 0.006852

omega 0.000001 0.000001 0.879222 0.379281

alpha1 0.000000 0.009631 0.000018 0.999986

beta1 0.943001 0.013853 68.069707 0.000000

gamma1 0.082897 0.019106 4.338717 0.000014

Robust Standard Errors:

Estimate Std. Error t value Pr(>|t|)

mu 0.000245 0.000157 1.559756 0.118818

ar1 -0.074942 0.023622 -3.172597 0.001511

omega 0.000001 0.000015 0.063334 0.949501

alpha1 0.000000 0.048887 0.000004 0.999997

beta1 0.943001 0.155045 6.082123 0.000000

gamma1 0.082897 0.149275 0.555334 0.578666

LogLikelihood : 4768.721

Information Criteria

------------------------------------

Akaike -6.8528

Bayes -6.8302

Shibata -6.8529

Hannan-Quinn -6.8444

Weighted Ljung-Box Test on Standardized Residuals

------------------------------------

> dlus.gjr

*---------------------------------*

* GARCH Model Fit *

*---------------------------------*

Conditional Variance Dynamics

-----------------------------------

GARCH Model : gjrGARCH(1,1)

Mean Model : ARFIMA(1,0,0)

Distribution : norm

Optimal Parameters

------------------------------------

Estimate Std. Error t value Pr(>|t|)

mu 0.000245 0.000183 1.340180 0.180187

ar1 -0.074942 0.027716 -2.703945 0.006852

omega 0.000001 0.000001 0.879222 0.379281

alpha1 0.000000 0.009631 0.000018 0.999986

beta1 0.943001 0.013853 68.069707 0.000000

gamma1 0.082897 0.019106 4.338717 0.000014

Robust Standard Errors:

Estimate Std. Error t value Pr(>|t|)

mu 0.000245 0.000157 1.559756 0.118818

ar1 -0.074942 0.023622 -3.172597 0.001511

omega 0.000001 0.000015 0.063334 0.949501

alpha1 0.000000 0.048887 0.000004 0.999997

beta1 0.943001 0.155045 6.082123 0.000000

gamma1 0.082897 0.149275 0.555334 0.578666

LogLikelihood : 4768.721

Information Criteria

------------------------------------

Akaike -6.8528

Bayes -6.8302

Shibata -6.8529

Hannan-Quinn -6.8444

Weighted Ljung-Box Test on Standardized Residuals

------------------------------------

statistic p-value

Lag[1] 0.003938 0.9500

Lag[2*(p+q)+(p+q)-1][2] 0.453423 0.9744

Lag[4*(p+q)+(p+q)-1][5] 1.435205 0.8622

d.o.f=1

H0 : No serial correlation

Weighted Ljung-Box Test on Standardized Squared Residuals

------------------------------------

statistic p-value

Lag[1] 4.918 0.02658

Lag[2*(p+q)+(p+q)-1][5] 5.404 0.12381

Lag[4*(p+q)+(p+q)-1][9] 6.045 0.29308

d.o.f=2

Weighted ARCH LM Tests

------------------------------------

statistic p-value

Lag[1] 0.003938 0.9500

Lag[2*(p+q)+(p+q)-1][2] 0.453423 0.9744

Lag[4*(p+q)+(p+q)-1][5] 1.435205 0.8622

d.o.f=1

H0 : No serial correlation

Weighted Ljung-Box Test on Standardized Squared Residuals

------------------------------------

statistic p-value

Lag[1] 4.918 0.02658

Lag[2*(p+q)+(p+q)-1][5] 5.404 0.12381

Lag[4*(p+q)+(p+q)-1][9] 6.045 0.29308

d.o.f=2

Weighted ARCH LM Tests

------------------------------------

Statistic Shape Scale P-Value

ARCH Lag[3] 0.4768 0.500 2.000 0.4899

ARCH Lag[5] 0.9559 1.440 1.667 0.7461

ARCH Lag[7] 1.1364 2.315 1.543 0.8904

Nyblom stability test

------------------------------------

Joint Statistic: 122.7693

Individual Statistics:

mu 0.1306

ar1 0.1738

omega 12.7333

alpha1 0.3491

beta1 0.1656

gamma1 0.2125

Asymptotic Critical Values (10% 5% 1%)

Joint Statistic: 1.49 1.68 2.12

Individual Statistic: 0.35 0.47 0.75

Sign Bias Test

------------------------------------

Statistic Shape Scale P-Value

ARCH Lag[3] 0.4768 0.500 2.000 0.4899

ARCH Lag[5] 0.9559 1.440 1.667 0.7461

ARCH Lag[7] 1.1364 2.315 1.543 0.8904

Nyblom stability test

------------------------------------

Joint Statistic: 122.7693

Individual Statistics:

mu 0.1306

ar1 0.1738

omega 12.7333

alpha1 0.3491

beta1 0.1656

gamma1 0.2125

Asymptotic Critical Values (10% 5% 1%)

Joint Statistic: 1.49 1.68 2.12

Individual Statistic: 0.35 0.47 0.75

Sign Bias Test

------------------------------------

t-value prob sig

Sign Bias 1.559 0.11925

Negative Sign Bias 1.936 0.05303 *

Positive Sign Bias 1.467 0.14253

Joint Effect 9.124 0.02769 **

Adjusted Pearson Goodness-of-Fit Test:

------------------------------------

group statistic p-value(g-1)

1 20 77.88 4.293e-09

2 30 86.60 1.202e-07

3 40 100.36 2.610e-07

4 50 103.09 1.006e-05

Elapsed time : 1.177835

t-value prob sig

Sign Bias 1.559 0.11925

Negative Sign Bias 1.936 0.05303 *

Positive Sign Bias 1.467 0.14253

Joint Effect 9.124 0.02769 **

Adjusted Pearson Goodness-of-Fit Test:

------------------------------------

group statistic p-value(g-1)

1 20 77.88 4.293e-09

2 30 86.60 1.202e-07

3 40 100.36 2.610e-07

4 50 103.09 1.006e-05

Elapsed time : 1.177835

out<-data.frame()

omega<-1e-6

alpha<-1e-6

beta<-0.943001

gamma<-0.082897

ht<-seq(1,3)

for (ht1 in c(0.5,1,2)) {

i<-1

for (ut1 in -2:2) {

ht[i]<-omega+beta*ht1+alpha*ut1^2+gamma*ut1^2*sign(ut1<0)

i<-i+1

}

out<-rbind(out, ht)

}

names(out)<-c(-2, -1, 0, 1, 2)

row.names(out)<-c(0.5, 1, 2)

out

-2 -1 0 1 2

0.5 0.8030935 0.5543995 0.4715015 0.4715025 0.4715055

1 1.2745940 1.0259000 0.9430020 0.9430030 0.9430060

2 2.2175950 1.9689010 1.8860030 1.8860040 1.8860070

レバレッジ効果がある

(5)

- 11を選択

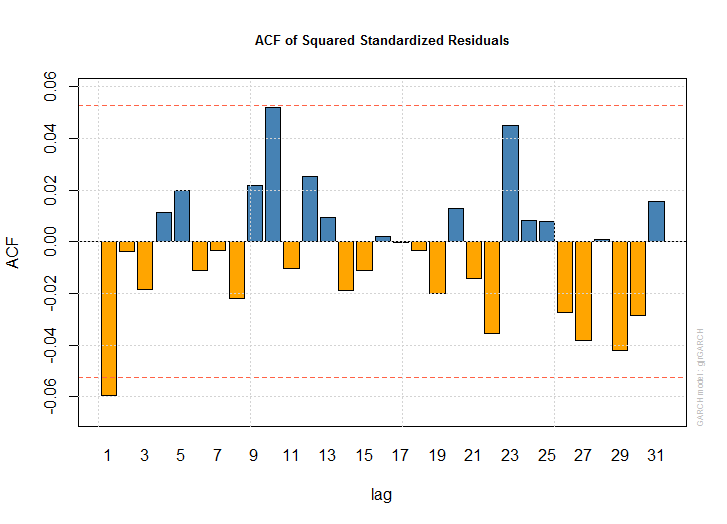

plot(dlus.garch)

plot(dlus.gjr)

(6)

dlus.spec<-ugarchspec(variance.model=list(model="eGARCH", garchOrder=c(1,1)), mean.model=list(armaOrder=c(1,0), include.mean=T))

dlus.egarch<-ugarchfit(data=dlus, spec=dlus.spec)

dlus.egarch

*---------------------------------*

* GARCH Model Fit *

*---------------------------------*

Conditional Variance Dynamics

-----------------------------------

GARCH Model : eGARCH(1,1)

Mean Model : ARFIMA(1,0,0)

Distribution : norm

Optimal Parameters

------------------------------------

Estimate Std. Error t value Pr(>|t|)

mu 0.000277 0.000195 1.4201 0.155567

ar1 -0.081870 0.032705 -2.5033 0.012304

omega -0.166643 0.002957 -56.3473 0.000000

alpha1 -0.087830 0.012714 -6.9080 0.000000

beta1 0.982551 0.000020 48090.9514 0.000000

gamma1 0.078968 0.000391 202.0952 0.000000

Robust Standard Errors:

Estimate Std. Error t value Pr(>|t|)

mu 0.000277 0.000214 1.2924 0.196233

ar1 -0.081870 0.034178 -2.3954 0.016601

omega -0.166643 0.003663 -45.4988 0.000000

alpha1 -0.087830 0.012832 -6.8448 0.000000

beta1 0.982551 0.000024 40637.8939 0.000000

gamma1 0.078968 0.000521 151.5471 0.000000

LogLikelihood : 4767.201

Information Criteria

------------------------------------

Akaike -6.8506

Bayes -6.8280

Shibata -6.8507

Hannan-Quinn -6.8422

Weighted Ljung-Box Test on Standardized Residuals

------------------------------------

statistic p-value

Lag[1] 0.005655 0.9401

Lag[2*(p+q)+(p+q)-1][2] 0.504447 0.9632

Lag[4*(p+q)+(p+q)-1][5] 1.590462 0.8240

d.o.f=1

H0 : No serial correlation

Weighted Ljung-Box Test on Standardized Squared Residuals

------------------------------------

statistic p-value

Lag[1] 4.386 0.03624

Lag[2*(p+q)+(p+q)-1][5] 4.918 0.15978

Lag[4*(p+q)+(p+q)-1][9] 5.652 0.34020

d.o.f=2

Weighted ARCH LM Tests

------------------------------------

-----------------------------------

GARCH Model : eGARCH(1,1)

Mean Model : ARFIMA(1,0,0)

Distribution : norm

Optimal Parameters

------------------------------------

Estimate Std. Error t value Pr(>|t|)

mu 0.000277 0.000195 1.4201 0.155567

ar1 -0.081870 0.032705 -2.5033 0.012304

omega -0.166643 0.002957 -56.3473 0.000000

alpha1 -0.087830 0.012714 -6.9080 0.000000

beta1 0.982551 0.000020 48090.9514 0.000000

gamma1 0.078968 0.000391 202.0952 0.000000

Robust Standard Errors:

Estimate Std. Error t value Pr(>|t|)

mu 0.000277 0.000214 1.2924 0.196233

ar1 -0.081870 0.034178 -2.3954 0.016601

omega -0.166643 0.003663 -45.4988 0.000000

alpha1 -0.087830 0.012832 -6.8448 0.000000

beta1 0.982551 0.000024 40637.8939 0.000000

gamma1 0.078968 0.000521 151.5471 0.000000

LogLikelihood : 4767.201

Information Criteria

------------------------------------

Akaike -6.8506

Bayes -6.8280

Shibata -6.8507

Hannan-Quinn -6.8422

Weighted Ljung-Box Test on Standardized Residuals

------------------------------------

statistic p-value

Lag[1] 0.005655 0.9401

Lag[2*(p+q)+(p+q)-1][2] 0.504447 0.9632

Lag[4*(p+q)+(p+q)-1][5] 1.590462 0.8240

d.o.f=1

H0 : No serial correlation

Weighted Ljung-Box Test on Standardized Squared Residuals

------------------------------------

statistic p-value

Lag[1] 4.386 0.03624

Lag[2*(p+q)+(p+q)-1][5] 4.918 0.15978

Lag[4*(p+q)+(p+q)-1][9] 5.652 0.34020

d.o.f=2

Weighted ARCH LM Tests

------------------------------------

Statistic Shape Scale P-Value

ARCH Lag[3] 0.07761 0.500 2.000 0.7806

ARCH Lag[5] 1.23064 1.440 1.667 0.6659

ARCH Lag[7] 1.39694 2.315 1.543 0.8418

Nyblom stability test

------------------------------------

Joint Statistic: 2.5097

Individual Statistics:

mu 0.2007

ar1 0.1198

omega 0.2873

alpha1 1.2433

beta1 0.2688

gamma1 0.2354

Asymptotic Critical Values (10% 5% 1%)

Joint Statistic: 1.49 1.68 2.12

Individual Statistic: 0.35 0.47 0.75

Sign Bias Test

------------------------------------

t-value prob sig

Sign Bias 1.441 0.14975

Negative Sign Bias 1.967 0.04941 **

Positive Sign Bias 1.387 0.16578

Joint Effect 8.142 0.04317 **

Adjusted Pearson Goodness-of-Fit Test:

------------------------------------

group statistic p-value(g-1)

1 20 74.78 1.452e-08

2 30 83.45 3.577e-07

3 40 87.99 1.202e-05

4 50 119.64 7.685e-08

Elapsed time : 0.8469431

Statistic Shape Scale P-Value

ARCH Lag[3] 0.07761 0.500 2.000 0.7806

ARCH Lag[5] 1.23064 1.440 1.667 0.6659

ARCH Lag[7] 1.39694 2.315 1.543 0.8418

Nyblom stability test

------------------------------------

Joint Statistic: 2.5097

Individual Statistics:

mu 0.2007

ar1 0.1198

omega 0.2873

alpha1 1.2433

beta1 0.2688

gamma1 0.2354

Asymptotic Critical Values (10% 5% 1%)

Joint Statistic: 1.49 1.68 2.12

Individual Statistic: 0.35 0.47 0.75

Sign Bias Test

------------------------------------

t-value prob sig

Sign Bias 1.441 0.14975

Negative Sign Bias 1.967 0.04941 **

Positive Sign Bias 1.387 0.16578

Joint Effect 8.142 0.04317 **

Adjusted Pearson Goodness-of-Fit Test:

------------------------------------

group statistic p-value(g-1)

1 20 74.78 1.452e-08

2 30 83.45 3.577e-07

3 40 87.99 1.202e-05

4 50 119.64 7.685e-08

Elapsed time : 0.8469431

out<-data.frame()

omega<--0.166646

alpha<--0.087830

beta<-0.982551

gamma<-0.078968

ht<-seq(1,3)

for (ht1 in c(0.5,1,2)) {

i<-1

for (ut1 in -2:2) {

ht[i]<-omega+beta*ht1+alpha*ut1^2+gamma*ut1^2*sign(ut1<0)

i<-i+1

}

out<-rbind(out, ht)

}

names(out)<-c(-2, -1, 0, 1, 2)

row.names(out)<-c(0.5, 1, 2)

out

-2 -1 0 1 2

0.5 0.2891845 0.3157705 0.3246325 0.2368025 -0.0266875

1 0.7804600 0.8070460 0.8159080 0.7280780 0.4645880

2 1.7630110 1.7895970 1.7984590 1.7106290 1.4471390

-2 -1 0 1 2

0.5 0.2891845 0.3157705 0.3246325 0.2368025 -0.0266875

1 0.7804600 0.8070460 0.8159080 0.7280780 0.4645880

2 1.7630110 1.7895970 1.7984590 1.7106290 1.4471390

レバレッジ効果がある

(7)

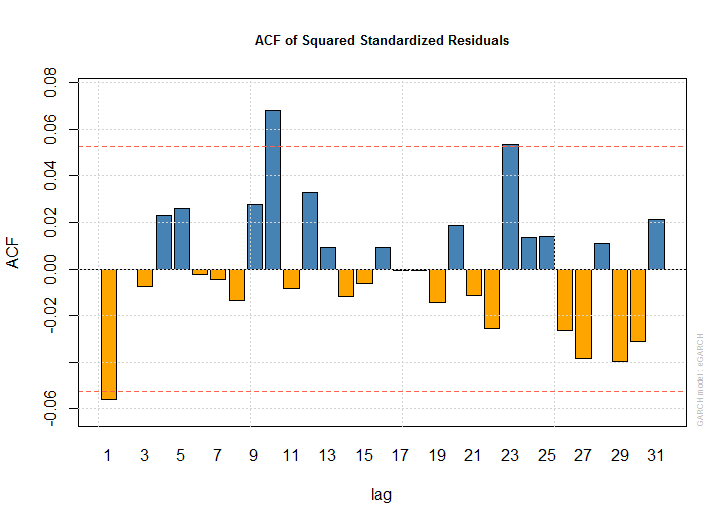

- 11を選択

plot(dlus.egarch)

(8)

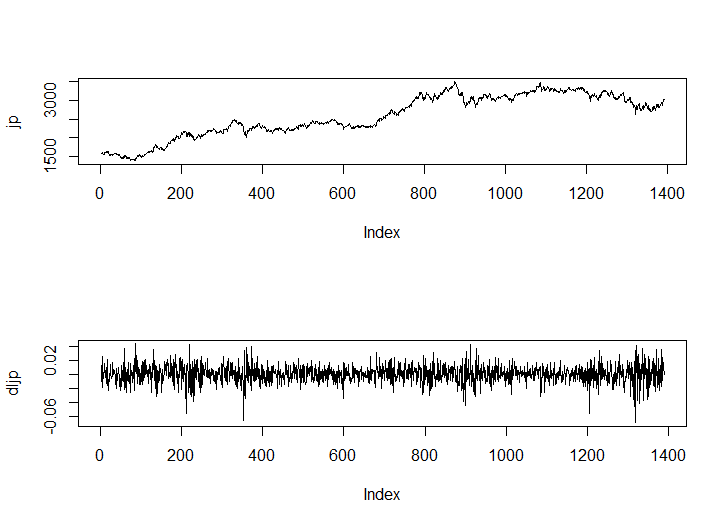

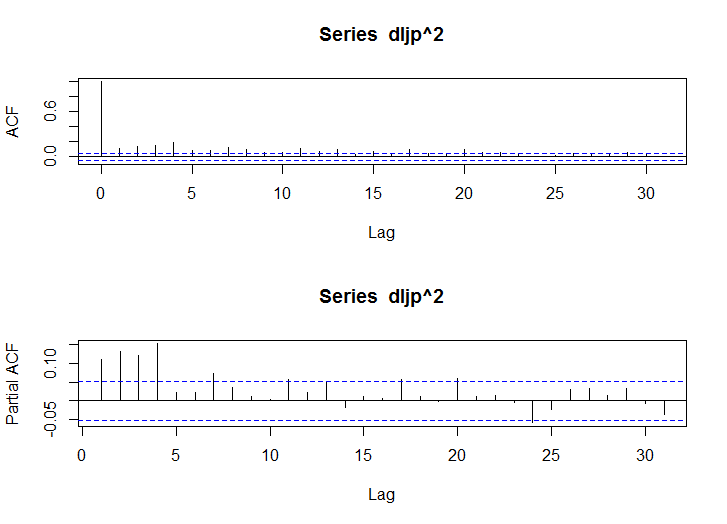

par(mfrow=c(2,1))

jp<-msci_day$jp

plot(jp, type="l")

dljp<-diff(log(jp))

plot(dljp, type="l")

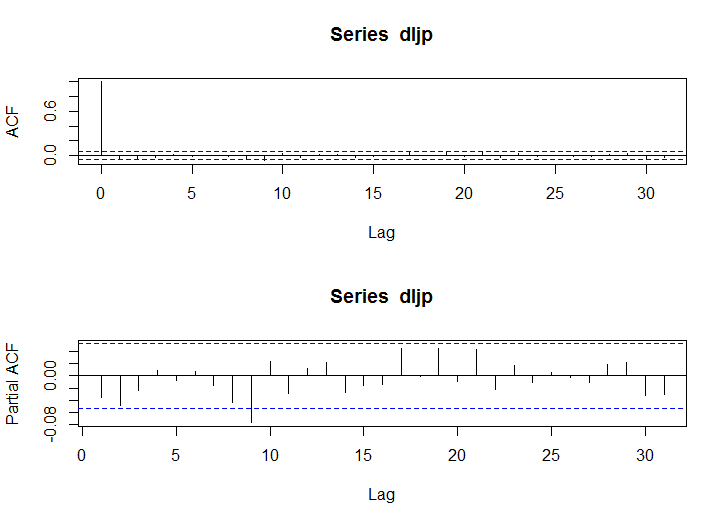

acf(dljp)

pacf(dljp)

acf(dljp^2)

pacf(dljp^2)

# GARCH

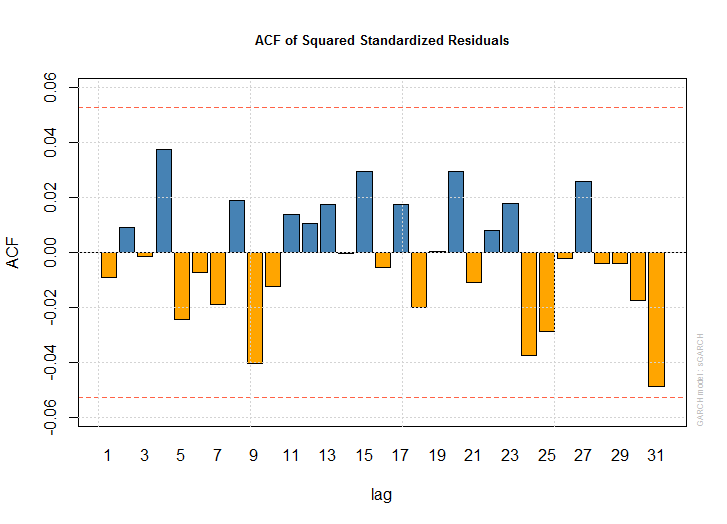

dljp.spec<-ugarchspec(variance.model=list(model="sGARCH", garchOrder=c(1,1)), mean.model=list(armaOrder=c(1,0), include.mean=T))

dljp.garch<-ugarchfit(data=dljp, spec=dljp.spec)

dljp.garch

*---------------------------------*

* GARCH Model Fit *

*---------------------------------*

Conditional Variance Dynamics

-----------------------------------

GARCH Model : sGARCH(1,1)

Mean Model : ARFIMA(1,0,0)

Distribution : norm

Optimal Parameters

------------------------------------

Estimate Std. Error t value Pr(>|t|)

mu 0.000566 0.000298 1.90212 0.057156

ar1 -0.010948 0.028309 -0.38675 0.698944

omega 0.000005 0.000003 1.39533 0.162918

alpha1 0.083277 0.003737 22.28493 0.000000

beta1 0.889458 0.011228 79.22073 0.000000

Robust Standard Errors:

Estimate Std. Error t value Pr(>|t|)

mu 0.000566 0.000282 2.00790 0.044653

ar1 -0.010948 0.025292 -0.43289 0.665098

omega 0.000005 0.000011 0.43276 0.665188

alpha1 0.083277 0.040851 2.03853 0.041497

beta1 0.889458 0.027516 32.32567 0.000000

LogLikelihood : 4150.981

Information Criteria

------------------------------------

Akaike -5.9654

Bayes -5.9466

Shibata -5.9655

Hannan-Quinn -5.9584

Weighted Ljung-Box Test on Standardized Residuals

------------------------------------

statistic p-value

Lag[1] 0.02266 0.8803

Lag[2*(p+q)+(p+q)-1][2] 1.08159 0.6901

Lag[4*(p+q)+(p+q)-1][5] 1.86771 0.7491

d.o.f=1

H0 : No serial correlation

Weighted Ljung-Box Test on Standardized Squared Residuals

------------------------------------

statistic p-value

Lag[1] 0.1186 0.7306

Lag[2*(p+q)+(p+q)-1][5] 1.1543 0.8239

Lag[4*(p+q)+(p+q)-1][9] 2.5367 0.8323

d.o.f=2

Weighted ARCH LM Tests

------------------------------------

Statistic Shape Scale P-Value

ARCH Lag[3] 0.002486 0.500 2.000 0.9602

ARCH Lag[5] 2.041177 1.440 1.667 0.4622

ARCH Lag[7] 2.500743 2.315 1.543 0.6123

Nyblom stability test

------------------------------------

Joint Statistic: 1.3237

Individual Statistics:

mu 0.12216

ar1 0.63447

omega 0.07506

alpha1 0.10576

beta1 0.12412

Asymptotic Critical Values (10% 5% 1%)

Joint Statistic: 1.28 1.47 1.88

Individual Statistic: 0.35 0.47 0.75

Sign Bias Test

------------------------------------

statistic p-value

Lag[1] 0.02266 0.8803

Lag[2*(p+q)+(p+q)-1][2] 1.08159 0.6901

Lag[4*(p+q)+(p+q)-1][5] 1.86771 0.7491

d.o.f=1

H0 : No serial correlation

Weighted Ljung-Box Test on Standardized Squared Residuals

------------------------------------

statistic p-value

Lag[1] 0.1186 0.7306

Lag[2*(p+q)+(p+q)-1][5] 1.1543 0.8239

Lag[4*(p+q)+(p+q)-1][9] 2.5367 0.8323

d.o.f=2

Weighted ARCH LM Tests

------------------------------------

Statistic Shape Scale P-Value

ARCH Lag[3] 0.002486 0.500 2.000 0.9602

ARCH Lag[5] 2.041177 1.440 1.667 0.4622

ARCH Lag[7] 2.500743 2.315 1.543 0.6123

Nyblom stability test

------------------------------------

Joint Statistic: 1.3237

Individual Statistics:

mu 0.12216

ar1 0.63447

omega 0.07506

alpha1 0.10576

beta1 0.12412

Asymptotic Critical Values (10% 5% 1%)

Joint Statistic: 1.28 1.47 1.88

Individual Statistic: 0.35 0.47 0.75

Sign Bias Test

------------------------------------

t-value prob sig

Sign Bias 0.3668 0.71379

Negative Sign Bias 0.8259 0.40900

Positive Sign Bias 1.8655 0.06233 *

Joint Effect 6.9489 0.07354 *

Adjusted Pearson Goodness-of-Fit Test:

------------------------------------

group statistic p-value(g-1)

1 20 26.43 0.11860

2 30 41.88 0.05751

3 40 46.26 0.19758

4 50 51.80 0.36520

Elapsed time : 1.276816

t-value prob sig

Sign Bias 0.3668 0.71379

Negative Sign Bias 0.8259 0.40900

Positive Sign Bias 1.8655 0.06233 *

Joint Effect 6.9489 0.07354 *

Adjusted Pearson Goodness-of-Fit Test:

------------------------------------

group statistic p-value(g-1)

1 20 26.43 0.11860

2 30 41.88 0.05751

3 40 46.26 0.19758

4 50 51.80 0.36520

Elapsed time : 1.276816

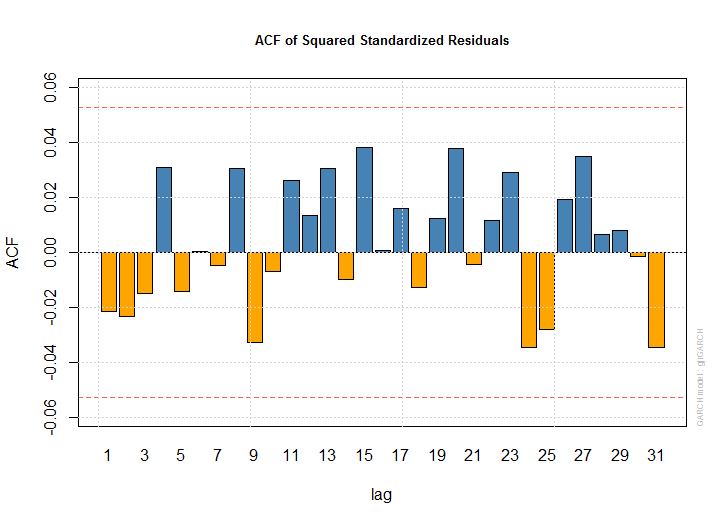

# GJR

dljp.spec<-ugarchspec(variance.model=list(model="gjrGARCH", garchOrder=c(1,1)), mean.model=list(armaOrder=c(1,0), include.mean=T))

dljp.gjr<-ugarchfit(data=dljp, spec=dljp.spec)

dljp.gjr

*---------------------------------*

* GARCH Model Fit *

*---------------------------------*

Conditional Variance Dynamics

-----------------------------------

GARCH Model : gjrGARCH(1,1)

Mean Model : ARFIMA(1,0,0)

Distribution : norm

Optimal Parameters

------------------------------------

Estimate Std. Error t value Pr(>|t|)

mu 0.000304 0.000304 0.999384 0.317609

ar1 -0.001567 0.028243 -0.055491 0.955747

omega 0.000007 0.000000 20.873872 0.000000

alpha1 0.017432 0.006800 2.563331 0.010367

beta1 0.877409 0.010546 83.198403 0.000000

gamma1 0.123741 0.025443 4.863400 0.000001

Robust Standard Errors:

Estimate Std. Error t value Pr(>|t|)

mu 0.000304 0.000282 1.07554 0.282131

ar1 -0.001567 0.026541 -0.05905 0.952912

omega 0.000007 0.000000 24.15722 0.000000

alpha1 0.017432 0.007349 2.37207 0.017689

beta1 0.877409 0.008430 104.07677 0.000000

gamma1 0.123741 0.031752 3.89708 0.000097

LogLikelihood : 4162.846

Information Criteria

------------------------------------

Akaike -5.9811

Bayes -5.9585

Shibata -5.9811

Hannan-Quinn -5.9726

Weighted Ljung-Box Test on Standardized Residuals

------------------------------------

*---------------------------------*

* GARCH Model Fit *

*---------------------------------*

Conditional Variance Dynamics

-----------------------------------

GARCH Model : gjrGARCH(1,1)

Mean Model : ARFIMA(1,0,0)

Distribution : norm

Optimal Parameters

------------------------------------

Estimate Std. Error t value Pr(>|t|)

mu 0.000304 0.000304 0.999384 0.317609

ar1 -0.001567 0.028243 -0.055491 0.955747

omega 0.000007 0.000000 20.873872 0.000000

alpha1 0.017432 0.006800 2.563331 0.010367

beta1 0.877409 0.010546 83.198403 0.000000

gamma1 0.123741 0.025443 4.863400 0.000001

Robust Standard Errors:

Estimate Std. Error t value Pr(>|t|)

mu 0.000304 0.000282 1.07554 0.282131

ar1 -0.001567 0.026541 -0.05905 0.952912

omega 0.000007 0.000000 24.15722 0.000000

alpha1 0.017432 0.007349 2.37207 0.017689

beta1 0.877409 0.008430 104.07677 0.000000

gamma1 0.123741 0.031752 3.89708 0.000097

LogLikelihood : 4162.846

Information Criteria

------------------------------------

Akaike -5.9811

Bayes -5.9585

Shibata -5.9811

Hannan-Quinn -5.9726

Weighted Ljung-Box Test on Standardized Residuals

------------------------------------

statistic p-value

Lag[1] 0.07495 0.7843

Lag[2*(p+q)+(p+q)-1][2] 0.99937 0.7403

Lag[4*(p+q)+(p+q)-1][5] 1.76512 0.7776

d.o.f=1

H0 : No serial correlation

Weighted Ljung-Box Test on Standardized Squared Residuals

------------------------------------

statistic p-value

Lag[1] 0.6437 0.4224

Lag[2*(p+q)+(p+q)-1][5] 2.0086 0.6164

Lag[4*(p+q)+(p+q)-1][9] 3.0480 0.7510

d.o.f=2

Weighted ARCH LM Tests

------------------------------------

Statistic Shape Scale P-Value

ARCH Lag[3] 0.3121 0.500 2.000 0.5764

ARCH Lag[5] 1.5248 1.440 1.667 0.5858

ARCH Lag[7] 1.6458 2.315 1.543 0.7917

Nyblom stability test

------------------------------------

Joint Statistic: 21.5161

Individual Statistics:

mu 0.2835

ar1 0.8198

omega 4.1418

alpha1 0.2854

beta1 0.2736

gamma1 0.1365

Asymptotic Critical Values (10% 5% 1%)

Joint Statistic: 1.49 1.68 2.12

Individual Statistic: 0.35 0.47 0.75

Sign Bias Test

------------------------------------

statistic p-value

Lag[1] 0.07495 0.7843

Lag[2*(p+q)+(p+q)-1][2] 0.99937 0.7403

Lag[4*(p+q)+(p+q)-1][5] 1.76512 0.7776

d.o.f=1

H0 : No serial correlation

Weighted Ljung-Box Test on Standardized Squared Residuals

------------------------------------

statistic p-value

Lag[1] 0.6437 0.4224

Lag[2*(p+q)+(p+q)-1][5] 2.0086 0.6164

Lag[4*(p+q)+(p+q)-1][9] 3.0480 0.7510

d.o.f=2

Weighted ARCH LM Tests

------------------------------------

Statistic Shape Scale P-Value

ARCH Lag[3] 0.3121 0.500 2.000 0.5764

ARCH Lag[5] 1.5248 1.440 1.667 0.5858

ARCH Lag[7] 1.6458 2.315 1.543 0.7917

Nyblom stability test

------------------------------------

Joint Statistic: 21.5161

Individual Statistics:

mu 0.2835

ar1 0.8198

omega 4.1418

alpha1 0.2854

beta1 0.2736

gamma1 0.1365

Asymptotic Critical Values (10% 5% 1%)

Joint Statistic: 1.49 1.68 2.12

Individual Statistic: 0.35 0.47 0.75

Sign Bias Test

------------------------------------

t-value prob sig

Sign Bias 0.4724 0.6367

Negative Sign Bias 0.4875 0.6260

Positive Sign Bias 0.8604 0.3897

Joint Effect 2.1598 0.5399

Adjusted Pearson Goodness-of-Fit Test:

------------------------------------

group statistic p-value(g-1)

1 20 25.08 0.1580

2 30 35.54 0.1874

3 40 36.42 0.5883

4 50 51.44 0.3785

Elapsed time : 0.350035

out<-data.frame()

omega<--0.361037

alpha<-0.017432

beta<-0.877409

gamma<-0.123741

ht<-seq(1,3)

for (ht1 in c(0.5,1,2)) {

i<-1

for (ut1 in -2:2) {

ht[i]<-omega+beta*ht1+alpha*ut1^2+gamma*ut1^2*sign(ut1<0)

i<-i+1

}

out<-rbind(out, ht)

}

names(out)<-c(-2, -1, 0, 1, 2)

row.names(out)<-c(0.5, 1, 2)

out

-2 -1 0 1 2

0.5 1.003403 0.5798845 0.4387115 0.4561435 0.5084395

1 1.442108 1.0185890 0.8774160 0.8948480 0.9471440

2 2.319517 1.8959980 1.7548250 1.7722570 1.8245530

-2 -1 0 1 2

0.5 1.003403 0.5798845 0.4387115 0.4561435 0.5084395

1 1.442108 1.0185890 0.8774160 0.8948480 0.9471440

2 2.319517 1.8959980 1.7548250 1.7722570 1.8245530

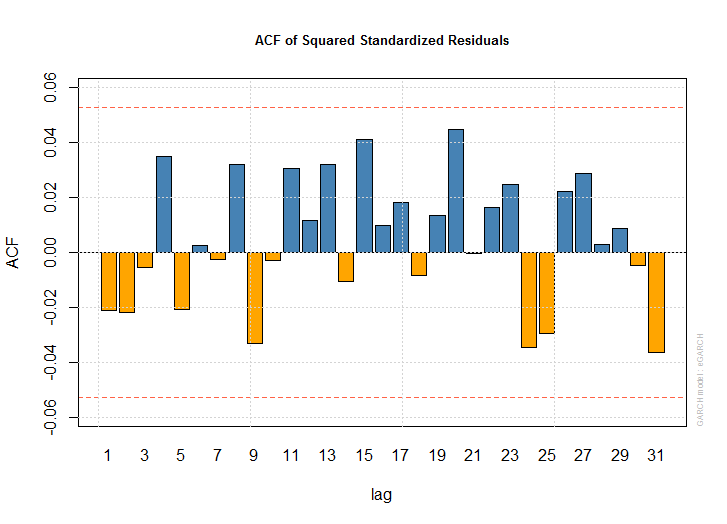

# EGARCH

dljp.spec<-ugarchspec(variance.model=list(model="eGARCH", garchOrder=c(1,1)), mean.model=list(armaOrder=c(1,0), include.mean=T))

dljp.egarch<-ugarchfit(data=dljp, spec=dljp.spec)

dljp.egarch

*---------------------------------*

* GARCH Model Fit *

*---------------------------------*

Conditional Variance Dynamics

-----------------------------------

GARCH Model : eGARCH(1,1)

Mean Model : ARFIMA(1,0,0)

Distribution : norm

Optimal Parameters

------------------------------------

Estimate Std. Error t value Pr(>|t|)

mu 0.000191 0.000377 0.50733 0.611924

ar1 -0.003791 0.029245 -0.12961 0.896873

omega -0.361037 0.232596 -1.55220 0.120614

alpha1 -0.088885 0.037871 -2.34705 0.018923

beta1 0.958573 0.026242 36.52825 0.000000

gamma1 0.168848 0.079853 2.11450 0.034473

Robust Standard Errors:

Estimate Std. Error t value Pr(>|t|)

mu 0.000191 0.000874 0.218611 0.82695

ar1 -0.003791 0.039681 -0.095524 0.92390

omega -0.361037 0.898477 -0.401832 0.68781

alpha1 -0.088885 0.134327 -0.661703 0.50816

beta1 0.958573 0.101299 9.462813 0.00000

gamma1 0.168848 0.309855 0.544926 0.58581

LogLikelihood : 4162.689

Information Criteria

------------------------------------

Akaike -5.9808

Bayes -5.9582

Shibata -5.9809

Hannan-Quinn -5.9724

Weighted Ljung-Box Test on Standardized Residuals

------------------------------------

statistic p-value

Lag[1] 0.1264 0.7222

Lag[2*(p+q)+(p+q)-1][2] 1.2006 0.6159

Lag[4*(p+q)+(p+q)-1][5] 2.0282 0.7032

d.o.f=1

H0 : No serial correlation

Weighted Ljung-Box Test on Standardized Squared Residuals

------------------------------------

statistic p-value

Lag[1] 0.6199 0.4311

Lag[2*(p+q)+(p+q)-1][5] 1.9735 0.6247

Lag[4*(p+q)+(p+q)-1][9] 3.1966 0.7261

d.o.f=2

Weighted ARCH LM Tests

------------------------------------

statistic p-value

Lag[1] 0.1264 0.7222

Lag[2*(p+q)+(p+q)-1][2] 1.2006 0.6159

Lag[4*(p+q)+(p+q)-1][5] 2.0282 0.7032

d.o.f=1

H0 : No serial correlation

Weighted Ljung-Box Test on Standardized Squared Residuals

------------------------------------

statistic p-value

Lag[1] 0.6199 0.4311

Lag[2*(p+q)+(p+q)-1][5] 1.9735 0.6247

Lag[4*(p+q)+(p+q)-1][9] 3.1966 0.7261

d.o.f=2

Weighted ARCH LM Tests

------------------------------------

Statistic Shape Scale P-Value

ARCH Lag[3] 0.04281 0.500 2.000 0.8361

ARCH Lag[5] 1.73869 1.440 1.667 0.5319

ARCH Lag[7] 1.91168 2.315 1.543 0.7360

Nyblom stability test

------------------------------------

Joint Statistic: 1.6343

Individual Statistics:

mu 0.32484

ar1 0.81875

omega 0.26270

alpha1 0.19614

beta1 0.26888

gamma1 0.02107

Asymptotic Critical Values (10% 5% 1%)

Joint Statistic: 1.49 1.68 2.12

Individual Statistic: 0.35 0.47 0.75

Sign Bias Test

------------------------------------

t-value prob sig

Sign Bias 0.1859 0.8525

Negative Sign Bias 0.4346 0.6640

Positive Sign Bias 1.0319 0.3023

Joint Effect 1.9371 0.5856

Adjusted Pearson Goodness-of-Fit Test:

------------------------------------

group statistic p-value(g-1)

1 20 33.02 0.0239

2 30 32.99 0.2780

3 40 41.02 0.3820

4 50 49.14 0.4676

Elapsed time : 0.663059

Statistic Shape Scale P-Value

ARCH Lag[3] 0.04281 0.500 2.000 0.8361

ARCH Lag[5] 1.73869 1.440 1.667 0.5319

ARCH Lag[7] 1.91168 2.315 1.543 0.7360

Nyblom stability test

------------------------------------

Joint Statistic: 1.6343

Individual Statistics:

mu 0.32484

ar1 0.81875

omega 0.26270

alpha1 0.19614

beta1 0.26888

gamma1 0.02107

Asymptotic Critical Values (10% 5% 1%)

Joint Statistic: 1.49 1.68 2.12

Individual Statistic: 0.35 0.47 0.75

Sign Bias Test

------------------------------------

t-value prob sig

Sign Bias 0.1859 0.8525

Negative Sign Bias 0.4346 0.6640

Positive Sign Bias 1.0319 0.3023

Joint Effect 1.9371 0.5856

Adjusted Pearson Goodness-of-Fit Test:

------------------------------------

group statistic p-value(g-1)

1 20 33.02 0.0239

2 30 32.99 0.2780

3 40 41.02 0.3820

4 50 49.14 0.4676

Elapsed time : 0.663059

out<-data.frame()

omega<-0.000191

alpha<--0.088884

beta<-0.958573

gamma<-0.168848

ht<-seq(1,3)

for (ht1 in c(0.5,1,2)) {

i<-1

for (ut1 in -2:2) {

ht[i]<-omega+beta*ht1+alpha*ut1^2+gamma*ut1^2*sign(ut1<0)

i<-i+1

}

out<-rbind(out, ht)

}

names(out)<-c(-2, -1, 0, 1, 2)

row.names(out)<-c(0.5, 1, 2)

out

-2 -1 0 1 2

0.5 0.4381015 0.1982125 0.1182495 0.0293645 -0.2372905

1 0.9173880 0.6774990 0.5975360 0.5086510 0.2419960

2 1.8759610 1.6360720 1.5561090 1.4672240 1.2005690

-2 -1 0 1 2

0.5 0.4381015 0.1982125 0.1182495 0.0293645 -0.2372905

1 0.9173880 0.6774990 0.5975360 0.5086510 0.2419960

2 1.8759610 1.6360720 1.5561090 1.4672240 1.2005690

- 11を選択

plot(dljp.garch)

plot(dljp.gjr)

plot(dljp.egarch)

7.5

DVEC, BEKK, CCC

- 他のモデルの関数が分からずCCCモデルのみ

library(ccgarch)

msci_day<-read.table("msci_day.txt",header=T)

jp<-msci_day$jp

uk<-msci_day$uk

us<-msci_day$us

data<-as.matrix(msci_day[,6:8])

a<-c(0.003, 0.005, 0.001)

A<-diag(c(0.2, 0.3, 0.15))

B<-diag(c(0.79, 0.6, 0.8))

R<-matrix(c(cor(jp,jp), cor(jp,uk), cor(jp,us), cor(uk,jp), cor(uk,uk), cor(uk,us), cor(us,jp), cor(us,uk), cor(us,us)), 3, 3)

eccc.estimation(a, A, B, R, data, model="diagonal")

でよいと思うが、

Error in solve.default(H) :

system is computationally singular: reciprocal condition number = 1.26294e-21

Error in solve.default(H) :

system is computationally singular: reciprocal condition number = 1.26294e-21