An Introduction to Statistical Learningの第三章に相関係数を使う一例があったので,まとめます.

広告の投資(TV, Radio, Newspaper)と売上(Sales)関連性を示すデータ・セットを使っています.

CSVファイルをimportして,最初の5行を表示します.

%matplotlib inline

import pandas as pd

import statsmodels.formula.api as smf

import seaborn as sns

import matplotlib.pyplot as plt

advertising = pd.read_csv("http://www-bcf.usc.edu/~gareth/ISL/Advertising.csv", usecols=[1,2,3,4])

advertising.head()

このデータセットは200行あって,カラムは4つです.

advertising.shape

# 結果

# (200, 4)

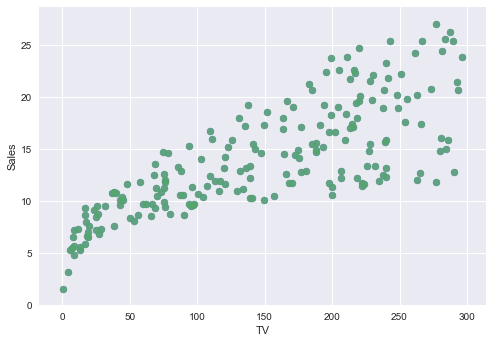

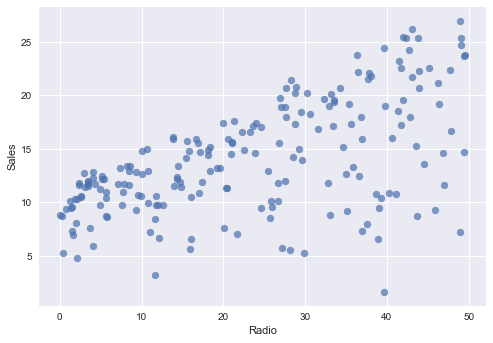

まずTV,Radio,NewspaperそれぞれSalesとの関連性をグラフで見てみます. それぞれのグラフのx軸は違うことに注意必要です.

TV ~ Sales

plt.scatter(advertising.TV , advertising.Sales, alpha=0.7)

plt.xlabel("TV")

plt.ylabel("Sales")

plt.show()

Radio ~ Sales

plt.scatter(advertising.Radio , advertising.Sales, alpha=0.7)

plt.xlabel("Radio")

plt.ylabel("Sales")

plt.show()

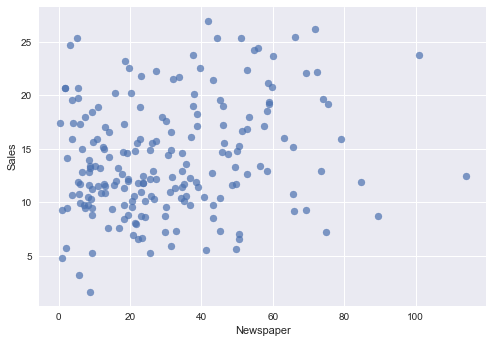

Newspaper ~ Sales

plt.scatter(advertising.Newspaper , advertising.Sales, alpha=0.7)

plt.xlabel("Newspaper")

plt.ylabel("Sales")

plt.show()

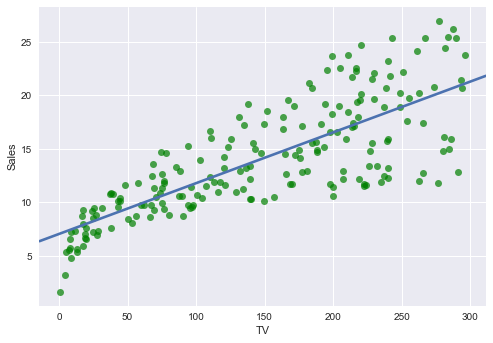

上の図を参考に仮にTV, Radio, NewspaperそれぞれSalesと線形回帰の関係もっているとします.グラフをプロットしてみます.

TV ~ Sales

sns.regplot(advertising.TV, advertising.Sales, ci=None, scatter_kws={'color':'g', 'alpha':0.7})

plt.xlabel("TV")

plt.ylabel("Sales")

plt.show()

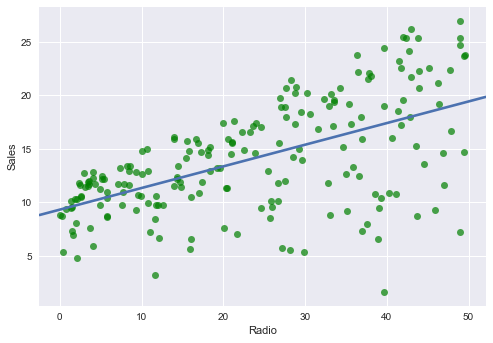

Radio ~ Sales

sns.regplot(advertising.Radio, advertising.Sales, ci=None, scatter_kws={'color':'g', 'alpha':0.7})

plt.xlabel("Radio")

plt.ylabel("Sales")

plt.show()

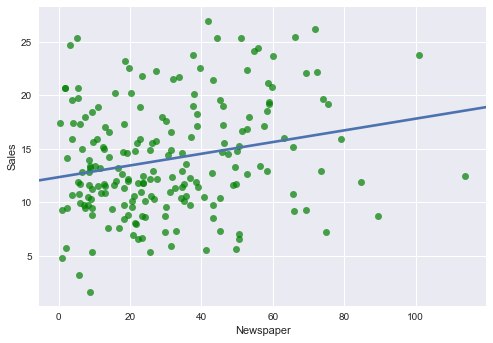

Newspaper ~ Sales

sns.regplot(advertising.Newspaper, advertising.Sales, ci=None, scatter_kws={'color':'g', 'alpha':0.7})

plt.xlabel("Newspaper")

plt.ylabel("Sales")

plt.show()

なんとなく TV〜Sales 回帰直線の傾きが大きいで, Newspaper〜Sales 回帰直線の傾きが小さいです.

TV ~ Sales回帰直線の傾き(coefficient)とy切片(intercept)をscikit learnのLinearRegressionで求めてみる.

from sklearn.linear_model import LinearRegression

reg = LinearRegression()

X = advertising.TV.values.reshape(-1,1)

y = advertising.Sales

reg.fit(X,y)

print("intercept: ", reg.intercept_)

print("coefficient: ", reg.coef_)

結果:

intercept: 7.03259354913

coefficient: [ 0.04753664]

Radio ~ Sales回帰直線の傾き(coefficient)とy切片(intercept)をscikit learnのLinearRegressionで求めてみる.

from sklearn.linear_model import LinearRegression

reg = LinearRegression()

X = advertising.Radio.values.reshape(-1,1)

y = advertising.Sales

reg.fit(X,y)

print("intercept: ", reg.intercept_)

print("coefficient: ", reg.coef_)

結果:

intercept: 9.31163809516

coefficient: [ 0.20249578]

Newspaper ~ Sales回帰直線の傾き(coefficient)とy切片(intercept)をscikit learnのLinearRegressionで求めてみる.

from sklearn.linear_model import LinearRegression

reg = LinearRegression()

X = advertising.Newspaper.values.reshape(-1,1)

y = advertising.Sales

reg.fit(X,y)

print("intercept: ", reg.intercept_)

print("coefficient: ", reg.coef_)

結果:

intercept: 12.3514070693

coefficient: [ 0.0546931]

Newspaper ~ Sales回帰直線の傾き(coefficient)に注目すると, 0.0546931になっています.

つまりNewspaperへの広告投資はSalesへ貢献無視できない. でもホントそうなのかは検証してみたいです.

さっきTV,Radio,Newspaperそれぞれ単回帰をscikit learn検証しました.今回多重回帰で検証してみます.

from sklearn.linear_model import LinearRegression

reg = LinearRegression()

X = advertising[['TV', 'Radio', 'Newspaper']].as_matrix()

y = advertising.Sales

reg.fit(X,y)

print("intercept: ", reg.intercept_)

print("coefficient: ", reg.coef_)

結果:

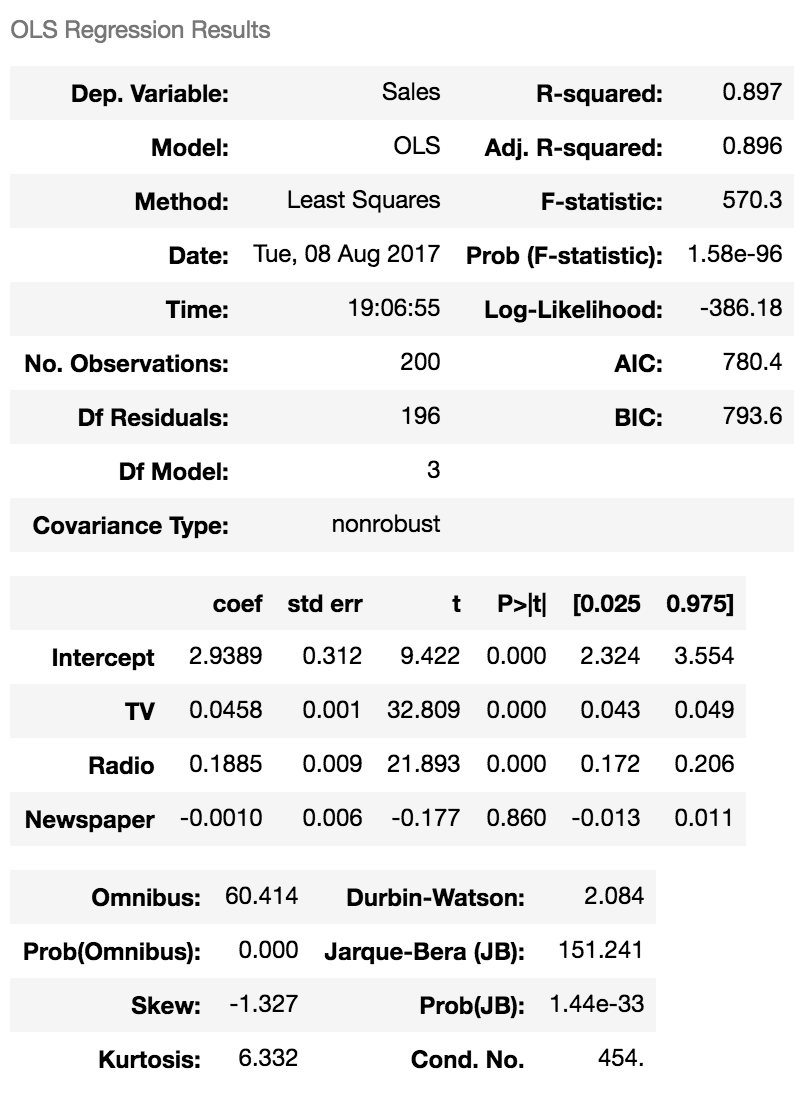

intercept: 2.93888936946

coefficient: [ 0.04576465 0.18853002 -0.00103749]

TV,Radioのcoefficientの部分さっき単回帰で検証した結果あんまり変わっていないです.

ここで興味深いのは Newspaperの coefficientは -0.00103749になりました.つまりNewspaperへの広告投資はSalseへの影響はないと? 実際はそうです.

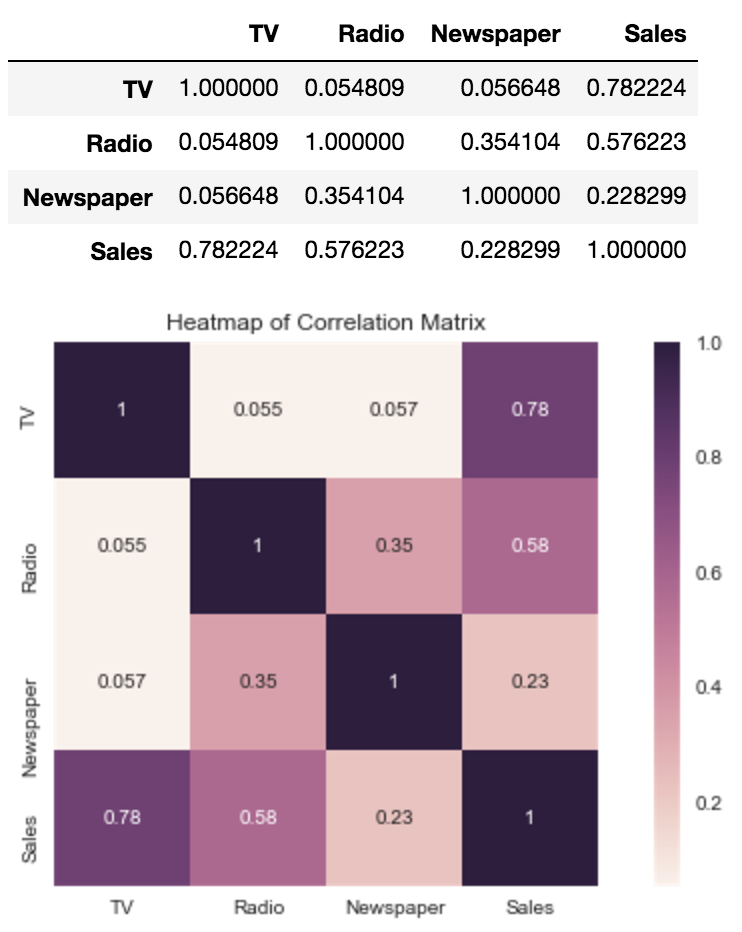

4つの変数の相関関係を見てみます. NewspaperとSalesの相関係数は一番小さいです.さらに NewspaperとRadioの相関係数0.354104は大きめです.Radioへの広告投資は多くなると,Newspaperへの広告投資も増えます. RadioとSalesの相関係数大きいです. つまりNewspaper〜Sales単回帰で求めたcoefficient 0.0546931実はRadioの恩恵を受けて,関連性あるように見えただけです.

単回帰は他の要素の影響を無視しているので,出てきた結論は一部間違いがあることがわかりました.

corr = advertising.corr()

plt.figure(figsize=(10,5))

sns.heatmap(corr,

xticklabels=corr.columns.values,

yticklabels=corr.columns.values,

vmax=1,

square=True,

annot=True

)

sns.plt.title('Heatmap of Correlation Matrix')

corr

さっきのinterceptとcoefficient見づらいなら,したの方法で求めることもできます. 下の2個目の表のNewspaperのp値0.860は非常に大きい値で, Newspaper〜Salesの間に関連性がないことの裏付けになります.

est = smf.ols('Sales ~ TV + Radio + Newspaper', advertising).fit()

est.summary()